Tagged: Biogen

COVID – 19 and its Effect on Convention Centers: Causes, Explanations and Thoughts on Recovery

Author’s Note: This is the first issue of The Convention Center Advisor that I’ve written for some time. I hope you find it informative.

I have just completed a book about managing convention centers titled. Improving Convention Center Management Using Business Analytics Key Performance Indicators. The book has two volumes, one focusing on fundamentals and the other on advanced practices. The book is published by Business Expert Press (BEP) and should be out now for sale. View a synopsis of the book on my website: http://www.conventioncenternow.com/look-inside-myles-mcgranes-new-book-improving-convention-center-management

To purchase the books, go to: Business Expert Press and click on the book covers.

January’s announcement restricting travel between the US and China was sobering but not serious enough to change our way of conducting business meetings. Then in late February, a biotechnology company, Biogen, held its annual leadership conference, One hundred and seventy – five executives gathered at the Marriott Long Wharf Hotel in Boston. The conference was spread across the multiple meeting rooms and ballrooms. There were research presentations, new product discussions, and business planning sessions. The conference also included scheduled group meals, coffee breaks, socializing and good fellowship. This setting belonged in our wheelhouse, in short the conference setting and service helped fulfill all the goals of a well-planned business meeting, Soon after the meeting ended, attendees and others associated with the event became ill. The ominous result was what medical researchers call a “super-spreader”. More than 90 people (Biogen managers and conference and guest service workers), became infected with the COVID -19 virus. The virus then spread throughout the Boston area and, as the virus’ hosts traveled home, to other states and on to parts of Europe, Asia and Australia.

Mass indoor gatherings where socializing is expected and encouraged are the ideal setting for virus spread. Indoors, the virus thrives on a crowd density which gives it a variety of available hosts over a short time period. More super spreading events followed in the spring and into summer from funerals to house parties and church choir practices. Then in late July the bell-weather of all live events, The Consumer Electronics Show in Las Vegas cancelled its January show. Other large events followed with cancellations; the National Association of Music Merchants Show, the Specialty Equipment Market Association Show, the Automotive Aftermarket Products Expo, and most recently the New York Toy Fair. Wisely most corporate events, tradeshows and association meetings, our clients, had already shut down or postponed operations. Convention centers were converted into field hospitals, supply and distribution centers, testing sites and even municipal court rooms. COVID – 19 was upon us.

Why Has the Exhibition Industry Been so Severely Affected?

The depth and profundity of COVID – 19 has brought about global economic instability. The arrival of the pandemic, just 12 years after the 2008 Recession, has affected all market sectors and all business functions. The result has been mass unemployment, huge government subsidies, deferred or cancelled investment plans, business failures, unpaid bills and sickness and death. The event industry cannot function in this environment. More familiar business risks such as, market risk or technology failure, seem insignificant now. The type of risk the world is experiencing today is called systematic risk by the investment community. Investopedia describes systematic risk as:

- Risk inherent to the market as a whole, reflecting the impact of a global economic breakdown like the Great Depression, political upheaval, or a war spread across many countries.

For certain, worldwide pandemics need to be included as a systematic risk. In this case a biological calamity suddenly and swiftly spread globally, slowing or shutting down the world’s economies.

- Unpredictable and difficult to avoid.

- Risk thatcan be somewhat mitigated if a company has a diversified lines of business

There are unambiguous and foundational causes for the rapid cancellations of conventions, conferences and tradeshows:

- The rapid spread of infection caused by everyday face to face communications. One can envision a convention or tradeshow being conducted today as if it were 2019 becoming a “super spreader”.

- The death rate of COVID – 19 for certain age groups and conditions

- Uncertainty about a new surge or “second wave” of infection much like the 1918 Flu pandemic

- Government shut down of all non-essential businesses and mass indoor gatherings

- The lack of therapeutic treatments and a preventive vaccine

- Re-purposing of convention and exhibiting facilities for emergency services; field hospitals, supply and distribution centers and testing sites for the virus

- Restrictions on interstate and international travel

Can Recovery for our Industry Be Forecast?

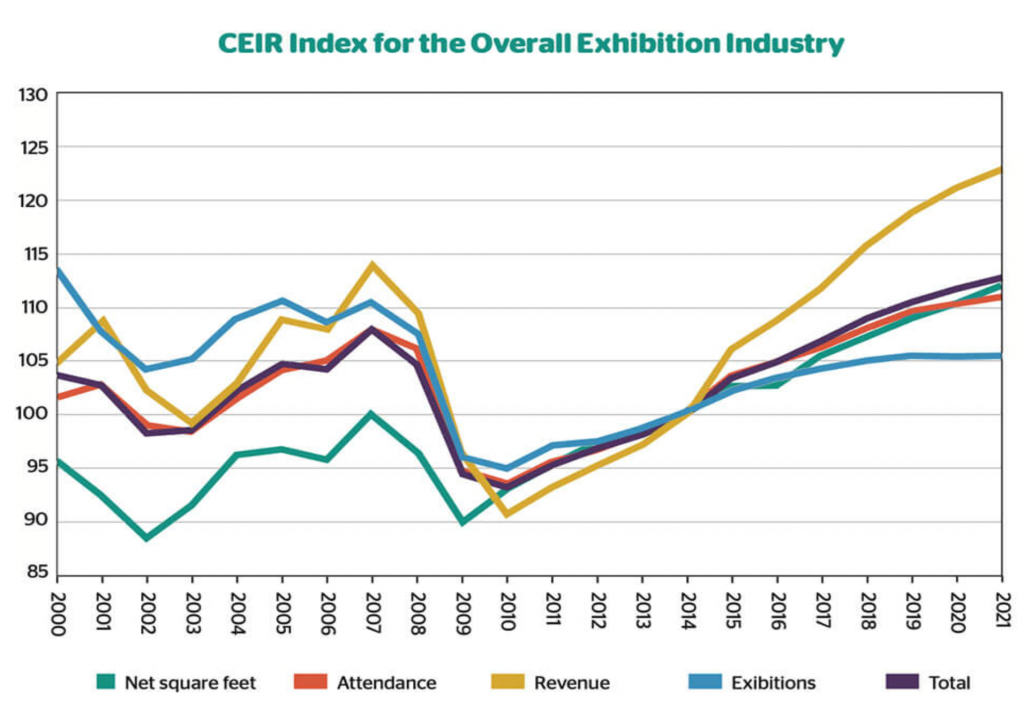

The state of the national economy has direct influence over our industry performance. As the economy advances or declines so do conventions, conferences and tradeshows. A useful measure of convention and tradeshow performance comes from the Center for Exhibition Industry Research. (CEIR). The CEIR Index is derived from key performance indicators from14 economic sectors. The indicators are; event net square footage, attendance, event organizer revenue and number of exhibiting companies. The index is the geometric mean of indicator values from all economic sectors.

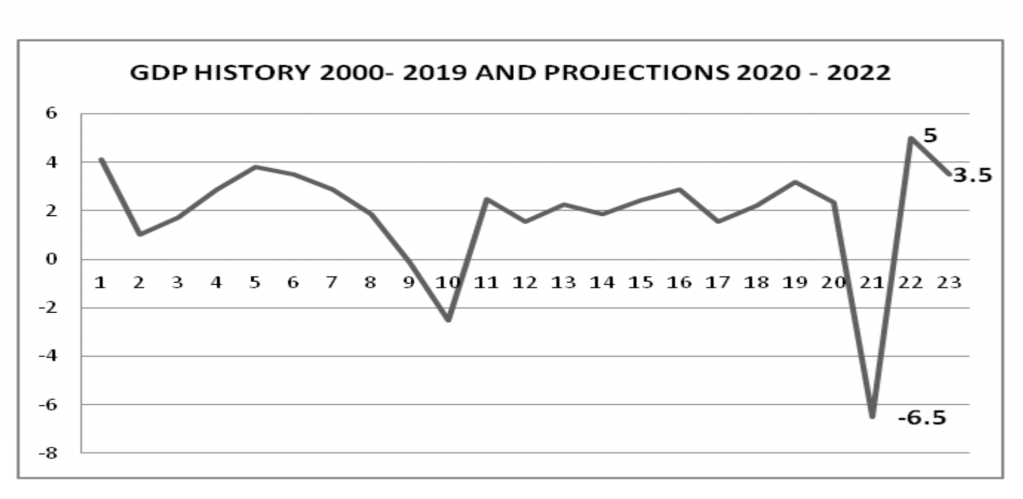

National economic performance is described using Gross Domestic Product (GDP). GDP is the sum of spending by consumers, government, and businesses plus net exports. It is expressed as a percentage change from one period (quarterly or annually) to the next.

The CEIR graphic below depicts the index performance from 2000 to 2019. The graphic was published before the pandemic so disregard forecasts for 2020 and 2021. Note the steep decline in 2001 to 2002, representing the 9/11 attack, and the same for 2008 to 2009, representing the Great Recession. Below the CEIR graphic is a line graph of annual Gross Domestic Product (GDP) for the same period.

Source: PCMA website, https://www.pcma.org/events-industry-forecast-exhibition-industry-evolves/

Source: US Bureau of Economic Analysis (BEA) and the Federal Reserve Open Market Committee’s June forecast

GDP and the CEIR Index components of net square footage, event attendees and number of exhibitors have moderate to strong correlations of .58, .75 and .52 respectively. This provides a statistical basis for GDP’s direct influence over our industry’s performance.

Although the units of measure are different for GDP and the CEIR Index components, there are other statistical similarities which tell a story. Most notable were the sharp drops in GDP due to global events. In the 4th quarter of 2001, just after the attack occurred, the GDP dropped to .15. The annual GDP for 2009, as the effect of the recession took hold, dropped to – 2.5. In 2nd quarter of 2020 GDP dropped to –31.7, the lowest recorded since the Great Depression. This portends a disastrous year for our industry. We already know this to be true.

The graphics also show that recovery of GDP and CEIR Index components begin at about the same time. However the shape of the recovery and the rate it progresses are very different. The GDP recovery was V shaped both after 9/11 and the 2008 Recession. The CEIR recovery is not V nor U shaped in either instance. Rather it is shaped like an exaggerated checkmark with the left side of the check showing a sharp decline and the right side curved and elongated. The inference is that the exhibition industry recovers at a slower pace than GDP after a global event.

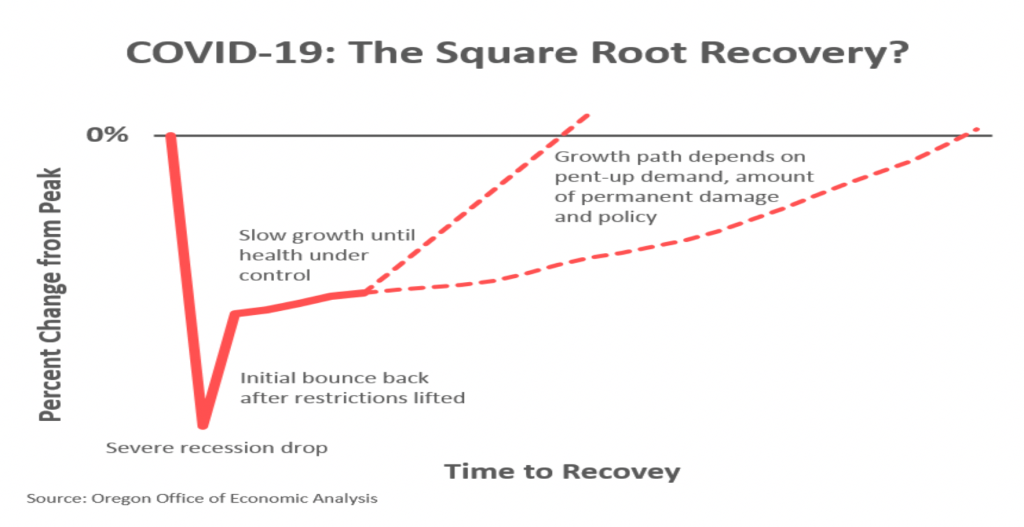

In the current pandemic however there are strong opinions that differ with the Federal Reserve Open Market Committee’s June forecast of a GDP V shaped recovery in 2021. In The Wall

Street Journal’s July Economic Forecasting Survey of Economists (reported in a blog published in the Yields-4u website), most surveyed believe US economic recovery would be shaped like the “Nike swoosh”. A smaller percentage believed it will be W shaped.

In the July Economic Forecasting Survey by The Wall Street Journal, which polls more than 60 U.S. economists each month, 13.0% of respondents thought the recovery would be V-shaped, 11.1% expected it to be W-shaped, 5.5% indicated it would be U-shaped, and none thought it would be L-shaped. The vast majority — 70.4% — believed the recovery would take a “Nike swoosh” shape, which suggests a sharp drop followed by a long, slow recovery. This view factors in the possibility that businesses may be slow to rehire, and consumers could be slow to resume pre-recession spending patterns. It also considers that some businesses may be impacted longer than others. Airlines do not expect to return to pre-COVID passenger activity until 2022, and movie theaters, beauty salons, sporting events, and other high-contact businesses may struggle until a vaccine is developed.

Economists and analysts elsewhere seem to favor the “swoosh” or checkmark recovery. The graphic below from the State of Oregon Office of Economic Analysis likened the shape to the square root symbol. They also offered this brief explanation of recovery: After we have control over the public health side of things, then the economic recovery may exhibit more of the classic U or V shapes depending on a variety of factors, including how much permanent damage is done during the recession, number of firms that fail, displaced labor, demand destruction, etc. – plus consumer’s pent up demand, monetary and fiscal policies and the like.

Source: https://oregoneconomicanalysis.com/2020/04/07/covid-19-the-square-root-recovery/

Beyond these explanations, for our industry the big question is whether and how the virus has fundamentally changed the way we conduct business.

“It’s tough to make predictions, especially about the future”. Yogi Berra was a wise man.

What Event Organizers Are Facing

For event organizers the recovery process will be complicated. I took time to join Event MB’s webinar “The Future of the Event Industry” a few weeks ago. I learned this:

- Small trade and consumer shows that have prospered pre- pandemic but have relied principally on cash flow and modest cash reserves have been forced to operate with minimal staff. Some have simply suspended event operations except for a small level of administrative activities. Launching virtual events where revenues are much less and hard to predict compared to live events is not a workable solution with this uncertain period. Theirs is a “wait and see” strategy.

- Large well – capitalized organizers have a much better chance of getting through this with their brand intact and the prospect of having live events again. Speakers at the webinar discussed the advantages of large event organizers and used Reed Exhibitions as an example. Reed is an operating unit of RELX, a global provider of information based analytics for businesses and professional clients. In December 2019 they were an 8.7 billion dollar company. Reed contributed 16% of that revenue and 13% profit. So RELX provides the strength and resiliency for Reed to ride out the pandemic. Being part of RELX provides the resources to engage in digital services for exhibitors such as, virtual product showcases and demonstrations, on-line lectures and education seminars, etc. The speakers believed that this form of thoughtful pro-active communication is necessary to keep the event brand fresh and exhibiting companies interested. Conversely, those event organizers unable to sustain the connection with exhibitors put themselves at considerable disadvantage making recovery more difficult.

The well – capitalized event organizers may have other things in mind if they don’t have to be concerned about declining revenues or the process of insolvency. There are no doubt smaller event organizers who are eager to sell assets to generate operating funds. Some of the assets may be events that fit well into a larger organizer’s portfolio. I expect any M & A activity to be a buyer’s market. With the absence of any organic growth, thoughtful acquisitions may be the only growth strategy.

There are other impediments for event organizers’ recovery efforts. Some are obvious but others have surfaced and are evolving:

- Event organizers willing to open a live or hybrid event have been confounded by some convention centers that remain closed so they can be used for emergency medical services should a second wave of the virus occur. There are others who are non – committal about opening for business or, as with McCormick Place, plan to stay closed until an effective vaccine is deployed.

- The business press hasn’t been helpful. An article in Barron’s (June 26th) was titled “Big Trade Shows Have All Been Cancelled. Why They May Never Come Back”. The article had plenty of examples. Here are two of them; at this year’s Apple Developer’s Conference nine million people watched Tim Cook’s keynote speech in an apparently flawless presentation from the Apple campus; a recent Cisco Live event had 125,000 virtual attendees vs. 28,000 attendees they expected at the live event. Also, Forbes Magazine through its Forbes Technology Council recently published a post titled, “Bringing the Value of Face-To-Face Interactions into Virtual Meetings, Briefings and Events”. The article stated that only 6% of exhibitors and 34% of attendees said trade shows had helped meet business objectives. Further, the author implied that B2B buyers (91%) prefer to consume interactive and visual content, opening the door to greater reach and awareness.

- In business as in physics “nature abhors a vacuum”. With no live events, technology in the form of virtual events has advanced to the point where elements of a trade show can achieved virtually and reasonably substitute for certain live experiences. Distance learning is a virtual format and has been in use frequently for conferences. The feature of interactivity has increased its popularity. However, virtual will be new for tradeshows and association events with exhibit booths. Many of us have read about or seen demos of virtual exhibit floors and booths but the concept never really made headway until now. The technology has vastly improved since introduced. I see virtual as a possible impediment to recovery due to the surge of advertising and media attention that virtual is currently receiving. The companies behind virtual events are not hesitant to promote virtual events as a new marketing method to rival and replace live events. Some of their arguments are persuasive, especially the cost of producing a virtual exhibit booth vs. all the costs associated with a live event. Some exhibiting companies will be persuaded to adopt the virtual methods of promoting their product and service. I believe, however, that there is too much technological risk and misplaced confidence that a screen image, even if interactive, can replicate being there, to speak directly to someone and engage the five senses. Organizers that already are or intend to use virtual during the pandemic know that the revenue model for virtual is much less than live. A recent CEIR blog described the difference as “trading dimes for dollars”. Organizers know however that virtual will have to play a part in future tradeshows and conventions. How can they integrate it properly into traditional event formats and effectively monetize its features?

Many event organizers are planning a combination live and virtual program they call “hybrid’ for possibly the 3rd quarter of 2021 for some the hybrid format is viewed as a means of keeping their larger exhibition on everyone’s business agenda and schedule until the pandemic is brought under control and mass indoor gatherings resume. If successful the hybrid format may become the preferred event format. This will be a difficult cultural transformation for some event organizers. The switch from a high density setting with crowded aisles, plentiful face to face interactions be it buying, selling, questioning, networking, etc., to a controlled and technology-based environment will take a level of organization and finesse that is not in their playbook. In the long run the benefits should outweigh the risks in producing a hybrid event. Virtual could be a valuable and innovative supplement for many trade shows and association conventions alike. Denzil Rankine, Chairman of the consultancy, AMR International believes that:

Virtual will not recreate the intimacy of live and not all tradeshows will be viewings of art fairs and other cancelled events replicating their main elements virtually will spread. Virtual will not be just about maintaining contact with communities in the case of cancellations. When normal business resumes virtual will have earned its place, extending reach both during and also between events.

Alternative virtual event formats are either in development or already launched. As an example, one event organization I follow is the American Society of Hematology (ASH). ASH is a not-for-profit professional association. They and like associations differ from privately owned and operated tradeshows in that earning revenue from the event is secondary to their mission of advocacy, professional standards and training and as a conduit for professional contacts and research. ASH’s annual meeting was originally scheduled for early December at the San Diego Convention Center. It was cancelled and replaced with a complete virtual program on the same dates. Their program is rich and comprehensive with a full schedule including; general sessions, presentations of scientific papers, workshops, symposia, continuing education and exhibitor and product showcases. In preparation for this article I talked with Bill Reed, ASH’s Chief Event Strategy Officer. He related the importance of this event to their scientific and medical community. Normally attendance approaches 30,000. It is the seminal gathering for this profession. The success of this virtual format is essential for ASH as they have other events throughout the year. ASH’s use of virtual may extend further into the future than other events. Because their annual meeting is for health science professionals, they will be very cautious about live events until real progress is made to stop COVID – 19 spread. Other health science events will probably think likewise.

- Airline industry business problems such as fewer direct flights and inconvenient schedules as well as reluctance by professionals to fly will not be solved easily.

- Not to be overlooked, there is the common sense element of fear of infection easily brought about by a trip to a live tradeshow or convention. Safe within their routine of a secure office or plant where health regulations are rigorously enforced, employees going to a live event in a distant city face an infection risk at the airport, in the airplane, the taxi, the hotel, the city streets, the convention center, perhaps a restaurant and then the same places as the process reverses. Why would a company or an individual take that risk or even consider it until a vaccine has been invented and proved effective?

What Convention Centers Are Facing

An objective view for convention centers sees a grim future stretching into the 3rd or 4th quarter of 2021. Indeed, the unpredictable severity of the virus’s second wave and the uncertain timing of a vaccine are maddening conditions. For convention centers, many have been told to suspend business operations in order to help manage second wave effects. Meanwhile complementary industries and businesses are struggling to survive; airlines, hotels, event service companies, restaurants, and more. .

Some of a convention center’s financial risk has been offset by reductions in payroll with lay-offs, furloughs and salary reductions. Certainly utility and supply costs have been reduced also. For some there may be rental revenue from housing all the medical and other emergency services during the height of the pandemic. For now the same subsidy payments that have always supported convention center capital and operating budgets are in place. In the short run, when events resume, expect them to be smaller with less exhibitors and attendees and less earned revenue from rent and services. In the long term however, convention centers face a more serious problem. The pandemic has caused steep and troubling drops in hotel occupancy. The Hotel News Resource website reported US hotel occupancy hit a low point in March of 22%, then climbed to a high point of 50.1% in mid August. Presently it is about 49%. The occupancy rate for early September 2019 was at 71%. When you combine corresponding declines in RevPar and ADR, the result is a serious decline in hotel occupancy tax collection.

For convention centers these taxes support three essential financial functions:

- Debt Service Payments (if the fund source for center construction was revenue bonds) -The revenue source is normally hotel occupancy taxes sometimes supplemented by car rental or restaurant tax. Bond holders have to rely on income generated by the project to make interest payments. The income is a portion of the price of a hotel room. Investors regard this as more risky than general obligation bonds and the bonds generally pay a higher interest rate.

- Funding Capital Improvements – For convention centers this is often an expansion of space or building renovations

- Covering Operating Deficits – Most of the convention centers in the US rely on revenue transferred from hotel tax receipts or some other form of subsidy like a state tourism fund to cover operating losses.

Starting in April news reports about decreasing hotel occupancy began to surface. Now every week there are news reports of fewer hotel guests. These reports often include commentary about cities or states concerned about using reserve funds to pay debt service for convention center bonds. If the bond sale was well structured the reserve funds are designed to continue debt interest payments through difficult periods. I know of no circumstance where convention center bonds have defaulted nor forced to use reserve funds to pay scheduled interest payments. But we’ve never faced such a severe economic downturn before. However bond market analysts are beginning to sound the alert. Below is an excerpt from a report written by S&P Global Ratings titled “Outlooks On Certain U.S. Convention Center And Sports Authorities Revised To Negative From Stable On COVID-19 Impact”:

…..a prolonged environment of limited to no operations will greatly hamper the entities’ ability to meet debt obligations, as they do not have other significant stable revenue streams to rely on and generally have limited local authority to raise new revenues. Although we expect convention center authorities will do everything in their power to create environments that are conducive to hosting large gatherings and using their facilities, including contingency planning, altering operations and budgets projections, and working with local, state, and federal officials, their ability to do so may be largely out of their control if the current crisis persists.

Convention center managers should be most concerned about the lack of capital funds and coverage of operating losses. What will happen if the pandemic continues to limit hotel occupancy? What will happen if debt service takes all the hotel occupancy tax receipts? What can the convention center do to support itself? Convention center management has tried to increase earned revenue from rent and service fees and commissions, therefore decreasing the need for subsidies to cover operating losses. Some have been successful and achieved positive cash flow consistently. Few have been able to build a capital reserve for building improvements. This will become a major dilemma, possibly long term.

A convention center’s path to recovery will follow a similar path and trajectory as the event organizers. Know that it’s probable as bookings resume and events re-schedule, that space requirements, number of exhibitors and attendees will be reduced. Some events may be of fewer days. Expect most attendees to come from regions within reasonable driving distance, so overnight hotel stays will be less.

A Plan for Convention Center Management in the Interim

Board chairmen, CEOs and general managers should sense that now is a good time to devise a plan. Business is slowly returning, GDP and employment growth will consistently improve and the vaccine news is mostly favorable.

- First things first; achieve GBAC or equivalent certification for facility safety and cleanliness

- Assemble your team, key department and division heads, not too large. As a starting point, Finance will present a thorough data based report on current financial status vs. plan before the pandemic. Sales will do likewise.

- Develop a list and fact based description of plausible scenarios. The scenarios should include an optimistic, pessimistic, a current momentum and a most likely case scenario. Each scenario should follow the same framework for issues and concerns outside the convention center’s control; the pandemic status, the vaccine development and deployment progress, government regulations and policy and the status of existing event clients. Example below:

Optimistic Scenario

COVID -19 – CDC forecasts a weak second wave for COVID – 19. However, they expressed concern about upcoming flu season and pressed states, regions and cities to aggressively promote flu vaccine shots within the next month

Vaccine – Trials are successful and deployment is ready to begin in the 1st quarter 2021

Gov’t – Restaurants will be cleared for indoor dining by 1st quarter 2021

Clients

- All of retained clients have made inquiries about resuming business in their normal date cycle by starting in late 2nd quarter 2021. Expect 15 -25% fewer exhibitors.

- Health Science events (there are 3) scheduled in 3rd and 4th quarter 2021 are still non – committal

- Lots of inquiries for consumer event clients, at least 20% more than 2018 and 2019.

4. Adapt the current business model (in place before the pandemic) to each scenario, Consideration should be given to the following:

- Expanding targeted markets to achieve greater occupancy. This “push everything through the front door” strategy is provocative and has risk, but such a compromise of sales strategy may be a necessity. You may be surprised what you find. A good example is how mid and small sized convention centers found certain indoor scholastic sports competitions a valuable market for earned revenue as well as out-of –town attendees.

- Review existing rent and service pricing. The market may well be highly competitive with competitors offering substantial discounts to regain market share.

- Review any capital funds remaining. Firstly, consider postponing any expansion plans you may have. You don’t need to build space you cannot fill. Think about improving the value of the space you have. Consider amending plans to accommodate expected event formats which have less exhibit space but more virtual and digital services. How can convention centers re-direct or obtain funding for improved communications infrastructure?

- Take on more services as building exclusives. This will cause controversy with event organizers who rely on commissions from service contractors they select. In the long run this is a fight worth fighting, especially with respect to high value services like electric. The convention center will need more revenue sources if subsidies become limited.

5. Plan on continually stress testing the business model adaptations against changing economic scenarios and frequent review of key performance indicators.

The Riddle of Pent Up Demand and the Sensibility of Face to Face Communication

Both pent up demand and face to face communications are inherent business concepts and part of our industry. There is no precise unit of measure to describe or quantify them, but there are available indicators that suggest their significance. I hope this narrative and explanation elicits an appreciation of their influence and importance.

Pent up demand is an inexact science but I know it exists in our industry..In my time at the Javits Center I experienced the power of pent up demand. The first time was when the business was reorganized in the mid 1990’s. At that time the center had an occupancy rate of about 39% trending downward. It was caused by a combination of corrupt, unproductive union labor and an absurd competitive event policy. The competitive event policy established long non-compete windows for existing events, in particular luxury goods, fashion and technology. Rapid reform of the labor issues and cancellation of the competitive event policy led to an occupancy rate of above 60% within two years and trending higher. Pent up demand came alive for us and did so dramatically. The second time was after 9/11. We had already begun to see strong weakening in net square footage use as a result of the dot- com bubble failure. In 2000 and 2001, the center

still had many technology sector clients as we witnessed their rapid decline. Then came 9/11. In the weeks following the attack we changed our marketing plan to include emphasis in other targeted event markets. The event inquiries and competition for dates were immediate. The result was 70% occupancy. I experienced pent up demand first hand but am ill-prepared to explain it properly. The thoughts and opinions of Scott Hoyt, a Senior Director at Moody’s Analytics, were helpful and are paraphrased below.

Pent-up demand is often discussed regarding consumer spending for durable goods such as appliances and automobiles. The US Bureau of Economic Analysis tracks these purchases nationwide and knows well the useful life of those products. When replacement spending does not meet forecast replacement as may happen during a recession, economists see this as a setting for pent up demand. The longer a consumer puts off buying a replacement, the stronger the desire to replace becomes. For other sectors such as business to business spending, there is no comparable unit of measure. However, a reasonable comparison can be made to the way consumer pent-up demand builds during a recession. Recessions are normally accompanied by higher household savings. Saving then falls during the recovery when consumers increase spending. This could easily compare with investors and large companies accumulating large cash reserves when there is high economic uncertainty as during a recession. The inference is that business spending behavior is similar to consumer spending behavior. In Scott Hoyt’s words, “consumers will lead the way.” Accepting that proposition, one can apply pent-up consumer demand for non-durable goods such as clothes and services such as vacations and discretionary medical procedures. Two services that come to mind are pricey vacations and going to the dentist. They are often put off during recessions, but come quickly back in focus as conditions improve.

There is another useful theory that uses the path spending would have taken with no recession. The approach assumes that income and employment had continued to grow and interest rates and unemployment were stable. So if CEIR forecasted 3.2% growth in the exhibition industry and a recession occurs, there would be a gap between forecasted and actual growth. Does the gap represent pent up demand? It is quite possible during a mild short lived recession, but our current economic downturn is so severe and long that profound changes in supply and demand would invalidate theory. It’s good to know what the target was though and use it as a benchmark. Pent up demand is an inexact science but I know it can be applied to our industry and its understanding will instruct and possibly guide us through recovery.

The Sensibility of Face to Face Communication

Face to face business dealings and transactions is a time honored concept dating back to the Middle Ages at mid-eastern bazaars or trade fairs in Europe. It has the quality of being able to see the other party close up and observe and read the way they express themselves not just through speech but also through facial expressions, body language and interactions with others. How else would one conduct business in an organized marketplace? The tradeshow, convention and consumer show is a business environment designed for personal contact and it has worked and grown successfully throughout the world.

Why is the emphasis on face to face communication so important? It’s not just the intimacy of speaking face to face. It’s also the direction a conversation can take, from the mundane to a shift for an esoteric idea that spontaneously grows into a business deal, an idea for a new product, an opportunity for business collaboration and more. It’s difficult to see this happening on Zoom. Some time ago Steve Jobs remarked that face to face communications would always be with us. He said, “There’s a temptation in our networked age to think that ideas can be developed by email and iChat. That’s crazy. Creativity comes from spontaneous meetings, from random discussions.”

There are other qualities and attributes of the role face to face communications plays at a tradeshow or convention:

- Communications is much clearer. It’s easy to misread and misinterpret information from a phone, email, text and even a video conference:

- Both verbal and non-verbal cues in a face to face meeting reveal something about the other party’s sincerity, trustworthiness and possibly more. These things are important and should cause you to research the facts and ideas from the conversation further.

- The conversation is more focused. The other party probably won’t be looking at personal messages on their cell phone as they probably do in a video conference.

- For a small business the opportunity to meet and talk leaders in the field and potential buyers of your product or service at a convention or tradeshow provides an accelerated path in marketing strategy

From The Plague by Albert Camus; “And indeed it could be said that once the faintest stirring of hope became possible, the dominion of plague was ended.”