Category: Uncategorized

In a Business Recovery Mode – Thoughts on a Convention Center’s Telephone/Internet Business Model

AUTHOR’S NOTE: This article was co-authored by Patrick Sarcinella. Patrick has over 25 years of event technology experience in the convention industry. His experience includes positions as Sr. Director of Sales for Millennium Technology Group (Rosen Hotels and Resorts) and Sr. Director of Southeast Operations with Smart City Networks, where he worked for over 16 years of his career, As part of this position Patrick led the Smart City team at the Orange County Convention Center.

The timing coincidence of two random events – the pandemic, and the other, the rapid success of groundbreaking improvements in wireless communications, have made the future of internet services at convention centers challenging.

As this issue of The Convention Center Advisor is being written, event market uncertainty persists. Convention centers have again been re-purposed from field hospitals, homeless shelters and COVID testing sites, to new roles as vaccination-sites and temporary shelters for unaccompanied migrant children. Until recently business reporting favored the dark side. Cancellations of leading sector events scheduled for Q2 2021 were reported regularly. Economic consultants serving CVBs and tradeshows were predicting a return to pre-pandemic event numbers anywhere from 2022 to as late as 2024. Grim forecasts for the airline and hotel sectors also portended an uncertain recovery. The International Air Transport Association (IATA) reported that US domestic air travel was down 65% from 2019 with return to pre-pandemic levels coming in 2024. Hotels were also voicing a similar forecast. Reported by hotel data firm STR, the pandemic was projected to erase a decade’s worth of revenue per available room (RevPAR) gains with room demand and average daily rate (ADR) unlikely to bounce back to 2019 levels until 2023 and 2025.

Now that Q1 2021 has come to an end, there are positive industry news stories about events taking place, albeit smaller and often virtual. Last month at a conference for the Association of Performing Arts Professionals, Dr. Anthony Fauci expressed optimism that live concerts and festivals could return sometime this Fall. Most believe this news also applies to conferences, conventions, and tradeshows. Vaccination progress improves daily and is reflected in most market news. Normally circumspect Forbes Magazine, in a March 1st article titled “Trade Shows Will Regain Importance After the Covid-19 Pandemic”, predicted a healthy comeback for tradeshows. The writer, Bill Conerly, characterized it this way, “Companies, like bicyclists, can coast now and then, especially if they have good momentum and especially if their competition also coasts. However, when competitors start pedaling again (or peddling), companies that ignore trade shows will fall behind. The benefits of exhibiting will help trade shows and conventions to resume, though with some changes.” A more cautious tone was expressed in a recent Wall Street Journal article on March 14th. Some recognition was given to tradeshows which have been piloting events of reduced size as well as ‘hybrid’ events that combine live exhibits and virtual presentations. However, the Journal opined that tradeshows will not return to their pre- COVID levels until 2023. For us, in conversations with industry contacts there is talk of fewer event cancellations, the recall of furloughed employees, and renewed enthusiasm from the exhibiting community for resuming tradeshows. Nevada’s Governor just relaxed capacity limits for mass gatherings to 50%. Our sense is that consumer pent up demand is transforming from palpable to tangible, evidenced in part by a surge in discretionary spending and experiential activities like restaurant dining and travel. Let us hope the “animal spirits” that drive today’s stock markets will revitalize our industry as well.

Where Things Stand –Business Environment Considerations for Convention Center Communications Services (Telephone – Analog Wired and Cell Service, WiFi Service, Wired Internet Service)

Given this business environment, it’s time for convention centers to actively plan a re-opening strategy. The business consultancy, McKinsey, expressed it this way, “….,organizations are transitioning from their only agenda item being near term survival to peering through the fog of uncertainty, thinking about how to position themselves once the crisis has passed and things return to normal”. We all sense that the “new” normal will be quite different than 2019. As the recovery takes hold, we will see fewer events, smaller in size and less attended. Convention centers will have a multitude of challenges, some of a general business nature such as:

• Getting as many events as possible through the doors and regaining 2019 their market share of events.

• Reckoning with stark reductions in event service revenue due to fewer exhibitors and attendees. Also, expect demands for rent concessions from event organizers who have the advantage of a buyer’s market.

• Dealing with the possibility of reduced subsidies to support operating deficits and capital projects. One prime source, hotel occupancy tax receipts which are already at diminished levels, will have a difficult recovery.

Other challenges deal directly with the convention center’s phone and internet service:

• Having capital resources to catch up with the pace of digital technology innovations that have been popularized during the pandemic.

• Developing a plan that prepares for increased internet service demand due to growth forecasts in 5G mobile device ownership and use.

On an operational level:

– Improving the relatively poor WiFi quality of service experienced with slow speeds and lost connections.

– Dealing with sub – standard cell phone coverage in many parts of convention centers with degraded signal

strength and dropped calls. These problems are due to the facility’s dense concrete and steel construction or LEED approved glass exterior curtain walls.

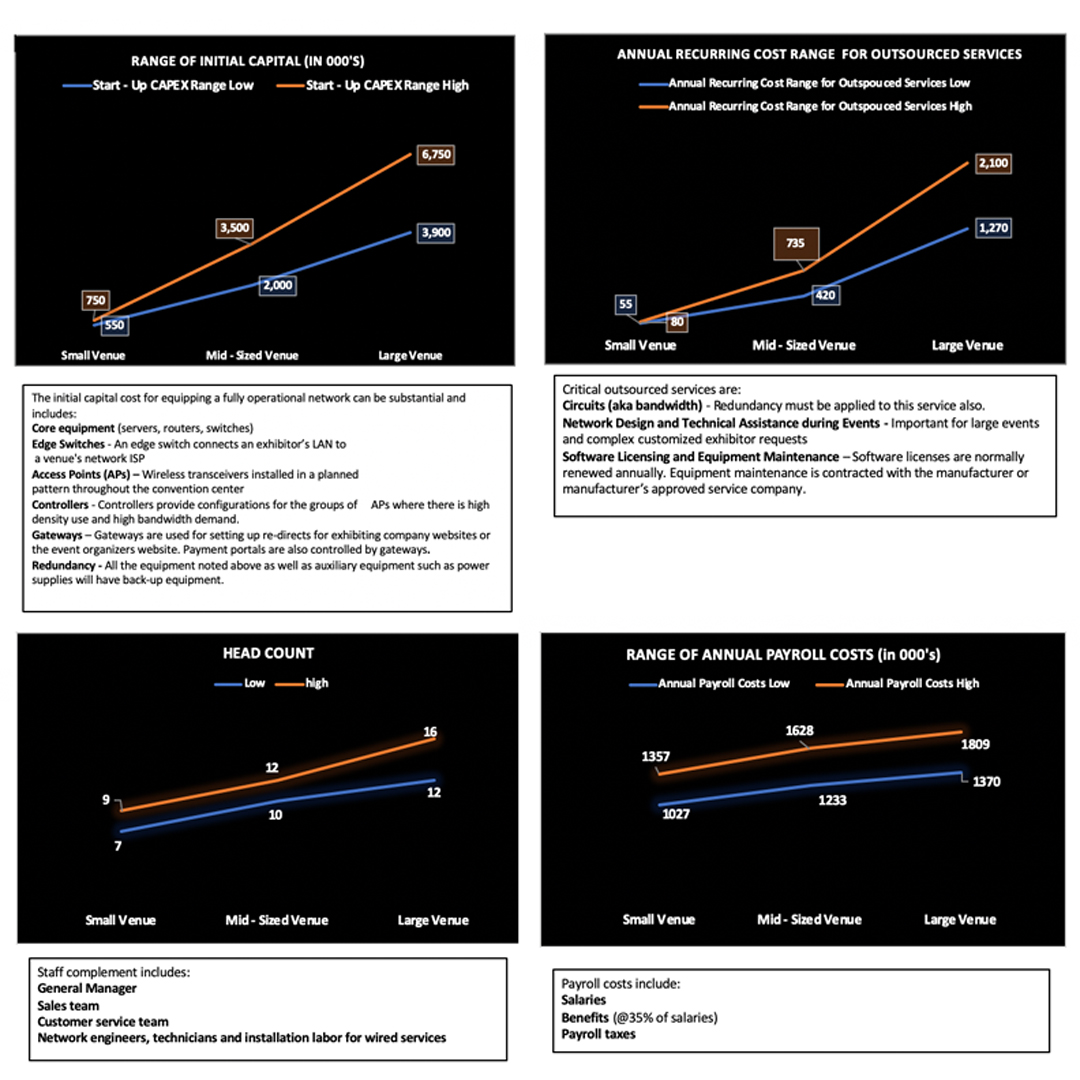

The graphics below depict the scale of capital and operations expenses for different size convention centers:

Pandemic Recovery – A Business Case for New Capital Investment

WiFi6

- The industry changed the naming of specific wireless internet services to something simpler and memorable. That means the technical standard, IEEE 802.11, became WiFi. and follow – on versions were named in sequence, so Wifi 4 became WiFi 5 and now WiFi 6. Within the standard for WiFi 6 is a feature called Orthogonal Frequency Division Multiple Access (OFDMA) which differentiates WiFi 6 from other WiFi versions in a material way. The feature solves convention center WiFi’s most vexing problem. It allows multiple users with varying bandwidth needs to be served simultaneously from APs without the nuisance of slow speeds or sudden loss of connection. It supports earlier WiFi versions with better performance and provides a platform for innovative applications, such as 4K video streaming, virtual reality, augmented reality and collaborative apps like Zoom and other video conferencing applications. In sum, WiFi 6 improves speed, capacity, and control.

- With technical problems solved, business will improve. It is reasonable to assume that a WiFi 6 equipped venue will likely generate more revenue and improve customer confidence in WiFi quality. It is also plausible that a WiFi 6 venue may have a competitive advantage for booking certain technology events.

- WiFi 6 is commercially viable. Many large venues, particularly stadiums, have installed WiFi 6. Examples are, Ohio State Stadium – Columbus, Lucas Oil Stadium – Indianapolis and Nissan Stadium – Nashville. As of this writing we do not know if WiFi 6 has been installed in any convention centers.

- Making an investment in WiFi 6 as we come out of the pandemic is a smart way of preparing for a surge in WiFi demand. The surge will follow close behind growth of 5G mobile device ownership. Services such as 4K streaming will become commonplace and you should expect event exhibitors and attendees to use them routinely.

- The cost of WiFi 6 can be managed and be gradual. The overall cost has a wide range based in part on the continued use of some WiFi 4 or 5 equipment and communications cable. The purchasing power of the convention center (public venues often utilize the purchasing advantages of state contracts) or the purchasing power and leverage of an outsourced internet contractor like Smart City Networks or Cox Communications will also reduce costs. Know that an outsourced contractor would normally absorb the full cost. Using the cost per AP as a guide, a rough estimate should range from $500 to 1000 per AP. Each AP has an effective coverage of 1,500 to 1,750 square feet.

Note 1: Small and mid-sized convention centers that have a WiFi 4 or 5 system in place that satisfies WiFi demand and service levels for event organizers, exhibitors and attendees may want to delay the WiFi 6 investment until market penetration becomes widespread and therefore necessary.

Note 2: Read the section below titled “5G and the Combination of 5G with WiFi 6 and DAS”.

Improving Cell Service – Distributed Antenna System (DAS) and Small Cells

- A DAS or small cells will reduce weak signal strength and dropped calls. For most mid to large convention centers DAS is an elegant solution because it expands coverage, improves \ quality and eliminates capacity shortages. Smaller convention centers should look at small cell technology as an alternative to DAS. Small cells are less expensive than DAS.

- A well- designed DAS will enable the convention center to keep up with future advances in cellular technology.

- There are alternatives for funding a DAS or Small Cell. If your phone/internet service is self-operated, then we recommend a hybrid business arrangement where the entire process is outsourced and paid for by a DAS owner as an exclusive contractor. There are companies which focus almost exclusively on building out and operating cell sites on properties owned by others. The leading companies are Crown Castle, American Tower Corp., and SBA Communications. Together they own and operate over 100,000 cell sites. You also have choices if phone/internet service is outsourced. You can proceed as described above and have two outsourced exclusive contracts, one for DAS (installation, operations and maintenance) and the other for analog telephone and internet service. For administrative simplicity you could request your current exclusive Phone/Internet contractor to handle the entire transaction and take on the construction and operating responsibilities with the DAS owner and operator as a sub-contractor. Again, the entire process will be outsourced and paid for by others.

- The convention center will share in the revenue obtained by the cell owner and operator by renting DAS space to carriers such as, Verizon or AT&T.

- DAS is proven and commercially viable. Several convention centers have already installed and profited by it; Las Vegas Convention Center, the Javits Center, the San Diego Convention Center and more.

Note: Read the section below titled “5G and the Combination of 5G with WiFi 6 and DAS”

5G and the Combination of 5G with WiFi 6 and DAS

- If yours is a large convention center in a top tier city with a consistent occupancy rate of 50% or more, then it’s resolved. At some point, business demands will force your convention center to become a 5G venue.

- 5G uses higher frequency bands which support faster speeds (100 times faster than 4G), less latency, and the capacity to simultaneously handle more devices.

- 5G will enable convention centers to provide several advanced, provocative features that enhance events and exhibitor product demonstrations. Listed below are a few of them:

• Highly reliable connectivity in dense crowded space

• The ability to view ultra- high resolution 4K video calls. It will also support 8K video which is out of its R & D phase and will become commercially viable in the next few years.

• Greatly improved virtual environments which replicate reality in a compelling way with clarity and realism. Virtual Reality (VR) and Augmented Reality (AR) are two of these applications. - The combination of WiFi6 and 5G is technically compatible. For a convention center it would first require that the carriers be prepared to offer 5G in the convention center locale and provide the required circuits or bandwidth. Bandwidth costs will increase somewhat but service revenue will easily make up for it. Additionally, there may be equipment upgrade costs.

The benefits of combining WiFi 6 and 5G are best described in this Cisco infograph:

cisco.com/c/m/en_us/solutions/enterprise-networks/802-11ax-solution/nb-06-5-things-WiFi6-5G-infograph-cte-en.html - Be cautious. The combination of a DAS and 5G poses some uncertainty. An existing DAS with 4 or 5G compatible equipment will not support the higher frequencies that a carrier’s 5G network does. For convention centers that have a DAS in a 4G network and plan on becoming a 5G network we recommend that they consult with the DAS manufacturer to see if the current system can adapt or be converted to 5G. We doubt it can.

We found one venue that elected to have a 5G carrier operate with the knowledge that 5G features are only available at the lower frequency range. AT&T Stadium, owned and operated by the Dallas Cowboys, elected to do that in 2019. Their marketing literature is very enthusiastic about their network performance capability. It would be interesting to learn how they came to that decision. It appears the complete conversion from 4G to 5G venue requires a new 5G capable DAS. AT&T Stadium elected to continue with their 4G DAS, operate 5G level services at 4G frequency ranges and forfeit 5G high frequency connections. We believe this is the approach AT&T Stadium took and will probably be reviewed by other sports venues.

There is one serious critic, Cisco, which expressed concerns about the limiting 5G full capabilities by using a 4G DAS. In a recent white paper they said, “We feel the current set of multi-operator solutions are ill equipped to enable 5G to thrive indoors.” The core of the criticism is that this combination limits the scalability or growth potential of 5G. We presume this is because a 4G DAS cannot operate at the higher frequencies that 5G can. To read the entire white paper click the link below:

cisco.com/c/dam/en/us/solutions/collateral/service-provider/ultra-services-platform/5g-ran-indoor.pdf

If the plan is to install your first DAS then the system engineer must specify that the DAS works reliably as part of a 5G in-building network. - 5G is commercially viable if there is a 5G tower in the locale. There are at least 43 stadiums and arenas that are 5G venues. Among them are Citi Field in NYC (MLB – NY Mets), SoFi Stadium in Los Angeles (NFL – Rams and Chargers), and FedEX Forum, (NBA – Memphis Grizzlies). We know of only one convention center which is a 5G venue, the Los Angeles Convention Center.

Pandemic Recovery – A Business Case for Reviewing Internet Service Price Strategy

The FCC investigations in 2013 and 2014 and their 2015 Consent Decree about wireless internet “blocking” cast a pall over the business practices of exclusive internet contractors at convention centers. The Consent Decree affirmed the rights of public use of the internet, prohibited “blocking” and took actions against companies that practiced blocking tactics. Fines were assessed and the venue industry’s credibility as a whole was harmed. These outcomes surprised many convention center managers. In the end though, they recognized the root cause of this controversy as the perception of excessive pricing for wireless internet services. The FCC’s 2015 actions were soon joined by more albeit less dramatic difficulties. Objections about the lack of “free” WiFi arose where event attendees made comparisons to free WiFi available at public libraries and coffee houses like Starbucks. Event organizers were also vocal on this point. The other issues were more subtle and revolved around the generally poor performance of exhibit hall WiFi during large events with high demand. These trials put convention centers and their exclusive contractors in a tough defensive position. Rather than awkwardly defending themselves, they took the high road and proceeded to look for solutions and made changes. Free Wifi quickly became universally offered for “light business” purposes (checking email for example). Contractors continued to wrestle with WiFi performance issues and improvised as best they could while being limited by the current AP technology. This is where things stood at the beginning of 2020.

Now with the pandemic ebbing and business confidence building, an opportunity exists to review pricing strategy with the aim of understanding complaints and objections, preserving profit margins and, venue commissions if outsourced and making sensible changes for the future. Where do we start? How does one approach this in a disciplined way? See below:

- Understanding the Nature of Convention Center Pricing

• Nothing pleases convention center management more than to have event services operate profitably by:

– Offering fair pricing based in part on local and competitor market conditions

– Growing profit margins organically through sales of premium products and services at premium prices

• Event service prices are generally high for several reasons:

– One obvious reason is that the customer is in effect captive. License Agreement terms require event organizers to use in-house services and exclusive contractors.

– A convention center’s physical plant and utility infrastructure is robust in nature. The event industry depends on the scale of the facility, its supporting property elements and the enormous utility capacity and distribution. These characteristics make centers much more expensive to operate than other buildings.

– Most License Agreement terms require workers to be labor union members. Service work performed by union labor greatly affects price.

– For outsourced services event revenue is shared as commissions with the convention center

- Determining which Services are Regarded as Commodities or Premium

• Make professional judgments about which services are considered a commodity or premium. Commodity pricing should be applied to services which are common, comparatively easy to set up and is in a reasonable range of phone and internet services at other venues. Premium services have opposite attributes from commodity services. They require more programming and testing, take up higher bandwidth and are generally of higher value for exhibiting companies. Higher pricing for more complex and more valuable services is more widely accepted by exhibitors.

• For many exhibitors it’s easy to characterize the price for some services as a form of price gouging. This is especially true if the prices are far above industry averages for what an exhibitor may regard as rudimentary work. For convention centers and their exclusive contractors, it’s wise to have a menu of services that effectively mix commodity products and services with premium products and services. A smart mix presents opportunities to preserve profit goals and control exhibitor complaints and resentment. Easy- to- fulfill orders can be priced more reasonably where there is natural price sensitivity and, value added, customized services can be priced at premium levels. - Taking Inventory – Comparing Pricing for Each Service Category Among Competitors

• Calculate a mean and a median for each service category. For a self – operated unit, it’s always a good policy to set your prices slightly below the mean.

• If possible, list the percentage changes in price for each category over the past three to five years.

• Footnote if time and material charges are applied separately and in addition to service prices and if any sales or temporary utility taxes are applied.

• Obtain data on service order volume by each service category.

• Classify services as either commodities and premiums and make this a consideration when making price changes. - Reviewing Each Service’s Profit Margin

• Each service category has a profit margin which should remain relatively consistent over time. Margins comparing current data should be compared to the multi-year mean.

• Profit margin data should regularly be compared to their multi-year mean and median.

• Knowledge of margin data will reveal opportunities for controlling labor costs and assist in making data based decisions when revising prices. - Actionable Items to Consider

• Seriously consider going through steps 2 to 4 above.

• For outsourced services, hold service pricing at 2019 levels and, if services are outsourced, in turn roll back commissions for a time with the condition that the contractor presents a plan for new technology investments. This can be done by a contract amendment that specifies the amount or percentage and a schedule for the roll back.

• For self-operated phone/internet services hold service pricing to 2019 levels until business recovers measured by occupancy rate growth and/or recovery of 2019 occupancy rates.

• Think about offering a grand good will gesture to event exhibitors and attendees. Here is one; offer free WiFi up to 5 mbps in such areas such as food courts and lobby entrances. At these speeds video calls with applications like Facetime or Facebook Messenger and most SD Streaming videos will work. Our guess is that there will be an increase for paid higher speed services so exhibitors and attendees can view 4K streaming. Know that CNET recently reported Starbucks offers free WiFi at 51.16 mbps, Taco Bell 14.29, Arby’s 14.24 and Subway at 4.78 mbps.

• Both self- operated and outsourced operators alike should sharpen their marketing and service messaging to exhibitors. Focus on the following:

– Fully understanding your pricing power and confidently defending premium prices. Developing a business logic and technique to defend premium vs. critics and competitors.

– Launching innovative and differentiated services at premium prices. Experienced managers can introduce new technology and services that create genuine and proven value for event exhibitors and event organizers.

– Raising prices annually without losing demand.

COVID – 19 and its Effect on Convention Centers: Causes, Explanations and Thoughts on Recovery

Author’s Note: This is the first issue of The Convention Center Advisor that I’ve written for some time. I hope you find it informative.

I have just completed a book about managing convention centers titled. Improving Convention Center Management Using Business Analytics Key Performance Indicators. The book has two volumes, one focusing on fundamentals and the other on advanced practices. The book is published by Business Expert Press (BEP) and should be out now for sale. View a synopsis of the book on my website: http://www.conventioncenternow.com/look-inside-myles-mcgranes-new-book-improving-convention-center-management

To purchase the books, go to: Business Expert Press and click on the book covers.

January’s announcement restricting travel between the US and China was sobering but not serious enough to change our way of conducting business meetings. Then in late February, a biotechnology company, Biogen, held its annual leadership conference, One hundred and seventy – five executives gathered at the Marriott Long Wharf Hotel in Boston. The conference was spread across the multiple meeting rooms and ballrooms. There were research presentations, new product discussions, and business planning sessions. The conference also included scheduled group meals, coffee breaks, socializing and good fellowship. This setting belonged in our wheelhouse, in short the conference setting and service helped fulfill all the goals of a well-planned business meeting, Soon after the meeting ended, attendees and others associated with the event became ill. The ominous result was what medical researchers call a “super-spreader”. More than 90 people (Biogen managers and conference and guest service workers), became infected with the COVID -19 virus. The virus then spread throughout the Boston area and, as the virus’ hosts traveled home, to other states and on to parts of Europe, Asia and Australia.

Mass indoor gatherings where socializing is expected and encouraged are the ideal setting for virus spread. Indoors, the virus thrives on a crowd density which gives it a variety of available hosts over a short time period. More super spreading events followed in the spring and into summer from funerals to house parties and church choir practices. Then in late July the bell-weather of all live events, The Consumer Electronics Show in Las Vegas cancelled its January show. Other large events followed with cancellations; the National Association of Music Merchants Show, the Specialty Equipment Market Association Show, the Automotive Aftermarket Products Expo, and most recently the New York Toy Fair. Wisely most corporate events, tradeshows and association meetings, our clients, had already shut down or postponed operations. Convention centers were converted into field hospitals, supply and distribution centers, testing sites and even municipal court rooms. COVID – 19 was upon us.

Why Has the Exhibition Industry Been so Severely Affected?

The depth and profundity of COVID – 19 has brought about global economic instability. The arrival of the pandemic, just 12 years after the 2008 Recession, has affected all market sectors and all business functions. The result has been mass unemployment, huge government subsidies, deferred or cancelled investment plans, business failures, unpaid bills and sickness and death. The event industry cannot function in this environment. More familiar business risks such as, market risk or technology failure, seem insignificant now. The type of risk the world is experiencing today is called systematic risk by the investment community. Investopedia describes systematic risk as:

- Risk inherent to the market as a whole, reflecting the impact of a global economic breakdown like the Great Depression, political upheaval, or a war spread across many countries.

For certain, worldwide pandemics need to be included as a systematic risk. In this case a biological calamity suddenly and swiftly spread globally, slowing or shutting down the world’s economies.

- Unpredictable and difficult to avoid.

- Risk thatcan be somewhat mitigated if a company has a diversified lines of business

There are unambiguous and foundational causes for the rapid cancellations of conventions, conferences and tradeshows:

- The rapid spread of infection caused by everyday face to face communications. One can envision a convention or tradeshow being conducted today as if it were 2019 becoming a “super spreader”.

- The death rate of COVID – 19 for certain age groups and conditions

- Uncertainty about a new surge or “second wave” of infection much like the 1918 Flu pandemic

- Government shut down of all non-essential businesses and mass indoor gatherings

- The lack of therapeutic treatments and a preventive vaccine

- Re-purposing of convention and exhibiting facilities for emergency services; field hospitals, supply and distribution centers and testing sites for the virus

- Restrictions on interstate and international travel

Can Recovery for our Industry Be Forecast?

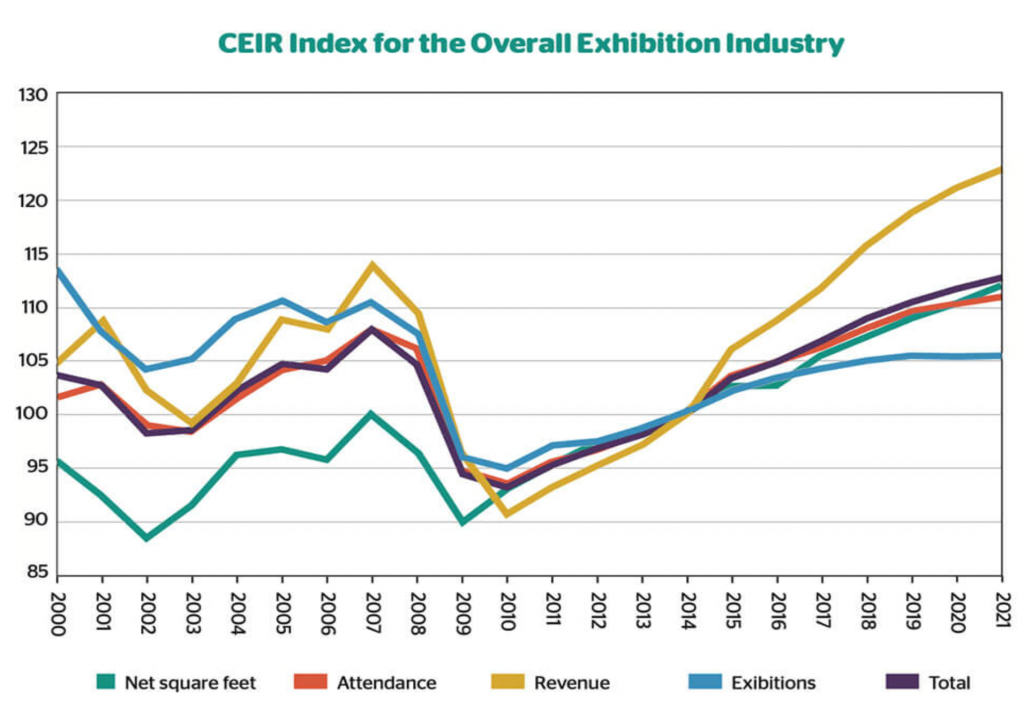

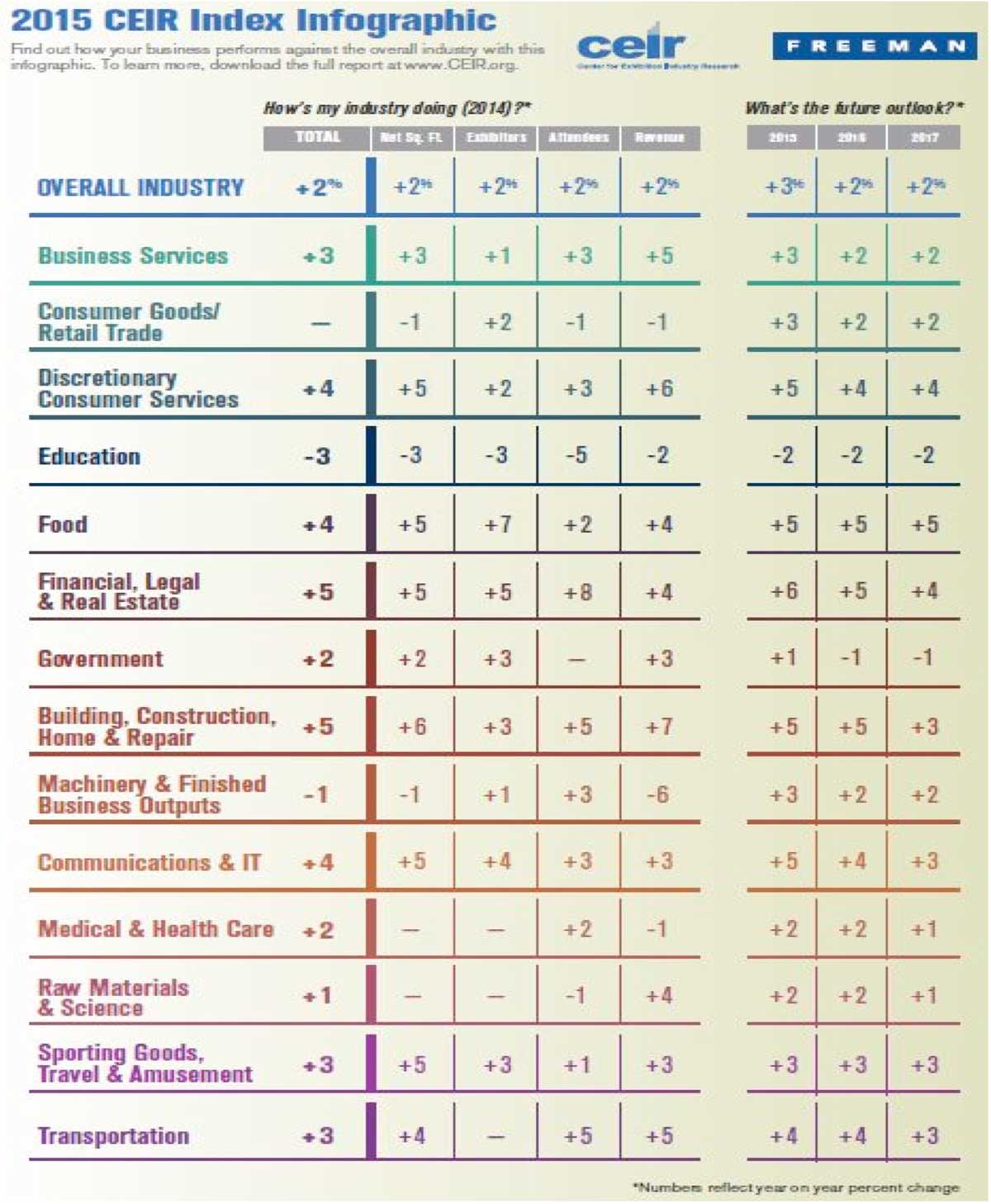

The state of the national economy has direct influence over our industry performance. As the economy advances or declines so do conventions, conferences and tradeshows. A useful measure of convention and tradeshow performance comes from the Center for Exhibition Industry Research. (CEIR). The CEIR Index is derived from key performance indicators from14 economic sectors. The indicators are; event net square footage, attendance, event organizer revenue and number of exhibiting companies. The index is the geometric mean of indicator values from all economic sectors.

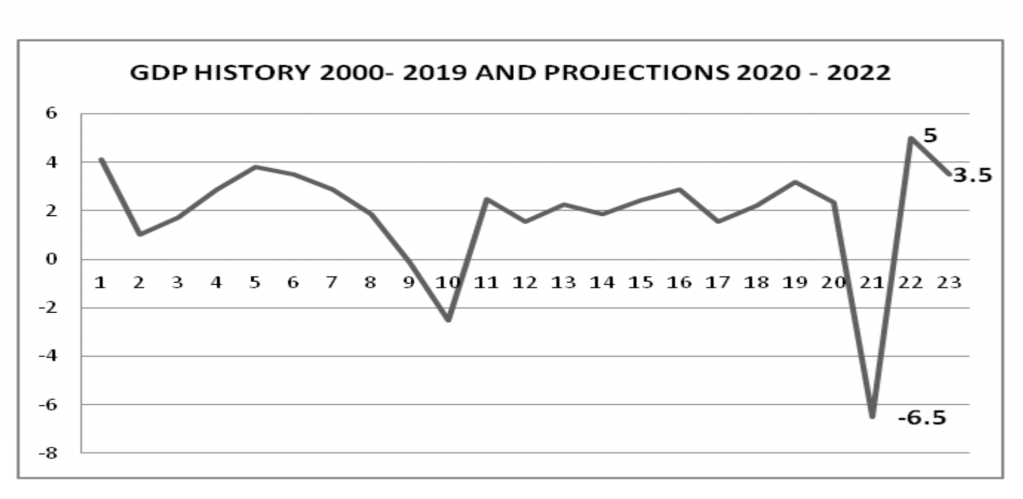

National economic performance is described using Gross Domestic Product (GDP). GDP is the sum of spending by consumers, government, and businesses plus net exports. It is expressed as a percentage change from one period (quarterly or annually) to the next.

The CEIR graphic below depicts the index performance from 2000 to 2019. The graphic was published before the pandemic so disregard forecasts for 2020 and 2021. Note the steep decline in 2001 to 2002, representing the 9/11 attack, and the same for 2008 to 2009, representing the Great Recession. Below the CEIR graphic is a line graph of annual Gross Domestic Product (GDP) for the same period.

Source: PCMA website, https://www.pcma.org/events-industry-forecast-exhibition-industry-evolves/

Source: US Bureau of Economic Analysis (BEA) and the Federal Reserve Open Market Committee’s June forecast

GDP and the CEIR Index components of net square footage, event attendees and number of exhibitors have moderate to strong correlations of .58, .75 and .52 respectively. This provides a statistical basis for GDP’s direct influence over our industry’s performance.

Although the units of measure are different for GDP and the CEIR Index components, there are other statistical similarities which tell a story. Most notable were the sharp drops in GDP due to global events. In the 4th quarter of 2001, just after the attack occurred, the GDP dropped to .15. The annual GDP for 2009, as the effect of the recession took hold, dropped to – 2.5. In 2nd quarter of 2020 GDP dropped to –31.7, the lowest recorded since the Great Depression. This portends a disastrous year for our industry. We already know this to be true.

The graphics also show that recovery of GDP and CEIR Index components begin at about the same time. However the shape of the recovery and the rate it progresses are very different. The GDP recovery was V shaped both after 9/11 and the 2008 Recession. The CEIR recovery is not V nor U shaped in either instance. Rather it is shaped like an exaggerated checkmark with the left side of the check showing a sharp decline and the right side curved and elongated. The inference is that the exhibition industry recovers at a slower pace than GDP after a global event.

In the current pandemic however there are strong opinions that differ with the Federal Reserve Open Market Committee’s June forecast of a GDP V shaped recovery in 2021. In The Wall

Street Journal’s July Economic Forecasting Survey of Economists (reported in a blog published in the Yields-4u website), most surveyed believe US economic recovery would be shaped like the “Nike swoosh”. A smaller percentage believed it will be W shaped.

In the July Economic Forecasting Survey by The Wall Street Journal, which polls more than 60 U.S. economists each month, 13.0% of respondents thought the recovery would be V-shaped, 11.1% expected it to be W-shaped, 5.5% indicated it would be U-shaped, and none thought it would be L-shaped. The vast majority — 70.4% — believed the recovery would take a “Nike swoosh” shape, which suggests a sharp drop followed by a long, slow recovery. This view factors in the possibility that businesses may be slow to rehire, and consumers could be slow to resume pre-recession spending patterns. It also considers that some businesses may be impacted longer than others. Airlines do not expect to return to pre-COVID passenger activity until 2022, and movie theaters, beauty salons, sporting events, and other high-contact businesses may struggle until a vaccine is developed.

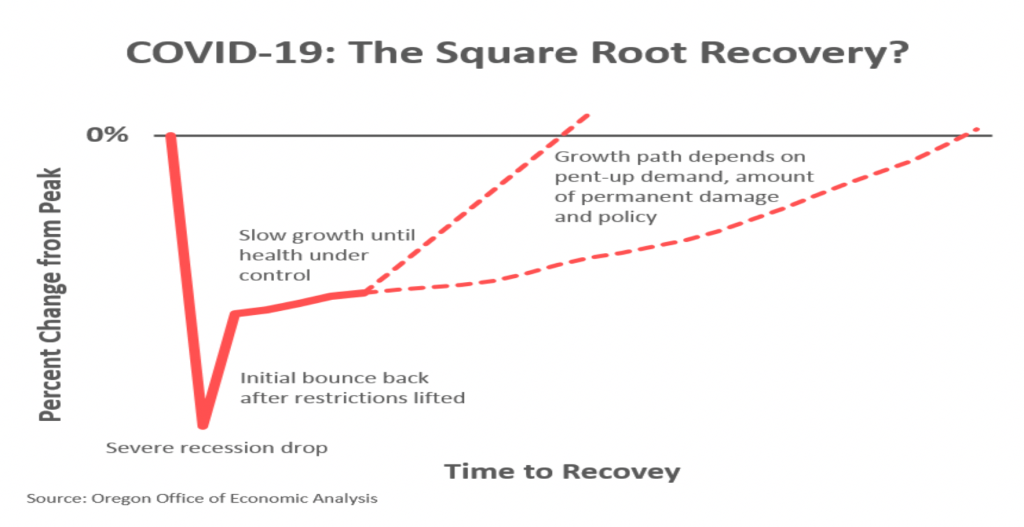

Economists and analysts elsewhere seem to favor the “swoosh” or checkmark recovery. The graphic below from the State of Oregon Office of Economic Analysis likened the shape to the square root symbol. They also offered this brief explanation of recovery: After we have control over the public health side of things, then the economic recovery may exhibit more of the classic U or V shapes depending on a variety of factors, including how much permanent damage is done during the recession, number of firms that fail, displaced labor, demand destruction, etc. – plus consumer’s pent up demand, monetary and fiscal policies and the like.

Source: https://oregoneconomicanalysis.com/2020/04/07/covid-19-the-square-root-recovery/

Beyond these explanations, for our industry the big question is whether and how the virus has fundamentally changed the way we conduct business.

“It’s tough to make predictions, especially about the future”. Yogi Berra was a wise man.

What Event Organizers Are Facing

For event organizers the recovery process will be complicated. I took time to join Event MB’s webinar “The Future of the Event Industry” a few weeks ago. I learned this:

- Small trade and consumer shows that have prospered pre- pandemic but have relied principally on cash flow and modest cash reserves have been forced to operate with minimal staff. Some have simply suspended event operations except for a small level of administrative activities. Launching virtual events where revenues are much less and hard to predict compared to live events is not a workable solution with this uncertain period. Theirs is a “wait and see” strategy.

- Large well – capitalized organizers have a much better chance of getting through this with their brand intact and the prospect of having live events again. Speakers at the webinar discussed the advantages of large event organizers and used Reed Exhibitions as an example. Reed is an operating unit of RELX, a global provider of information based analytics for businesses and professional clients. In December 2019 they were an 8.7 billion dollar company. Reed contributed 16% of that revenue and 13% profit. So RELX provides the strength and resiliency for Reed to ride out the pandemic. Being part of RELX provides the resources to engage in digital services for exhibitors such as, virtual product showcases and demonstrations, on-line lectures and education seminars, etc. The speakers believed that this form of thoughtful pro-active communication is necessary to keep the event brand fresh and exhibiting companies interested. Conversely, those event organizers unable to sustain the connection with exhibitors put themselves at considerable disadvantage making recovery more difficult.

The well – capitalized event organizers may have other things in mind if they don’t have to be concerned about declining revenues or the process of insolvency. There are no doubt smaller event organizers who are eager to sell assets to generate operating funds. Some of the assets may be events that fit well into a larger organizer’s portfolio. I expect any M & A activity to be a buyer’s market. With the absence of any organic growth, thoughtful acquisitions may be the only growth strategy.

There are other impediments for event organizers’ recovery efforts. Some are obvious but others have surfaced and are evolving:

- Event organizers willing to open a live or hybrid event have been confounded by some convention centers that remain closed so they can be used for emergency medical services should a second wave of the virus occur. There are others who are non – committal about opening for business or, as with McCormick Place, plan to stay closed until an effective vaccine is deployed.

- The business press hasn’t been helpful. An article in Barron’s (June 26th) was titled “Big Trade Shows Have All Been Cancelled. Why They May Never Come Back”. The article had plenty of examples. Here are two of them; at this year’s Apple Developer’s Conference nine million people watched Tim Cook’s keynote speech in an apparently flawless presentation from the Apple campus; a recent Cisco Live event had 125,000 virtual attendees vs. 28,000 attendees they expected at the live event. Also, Forbes Magazine through its Forbes Technology Council recently published a post titled, “Bringing the Value of Face-To-Face Interactions into Virtual Meetings, Briefings and Events”. The article stated that only 6% of exhibitors and 34% of attendees said trade shows had helped meet business objectives. Further, the author implied that B2B buyers (91%) prefer to consume interactive and visual content, opening the door to greater reach and awareness.

- In business as in physics “nature abhors a vacuum”. With no live events, technology in the form of virtual events has advanced to the point where elements of a trade show can achieved virtually and reasonably substitute for certain live experiences. Distance learning is a virtual format and has been in use frequently for conferences. The feature of interactivity has increased its popularity. However, virtual will be new for tradeshows and association events with exhibit booths. Many of us have read about or seen demos of virtual exhibit floors and booths but the concept never really made headway until now. The technology has vastly improved since introduced. I see virtual as a possible impediment to recovery due to the surge of advertising and media attention that virtual is currently receiving. The companies behind virtual events are not hesitant to promote virtual events as a new marketing method to rival and replace live events. Some of their arguments are persuasive, especially the cost of producing a virtual exhibit booth vs. all the costs associated with a live event. Some exhibiting companies will be persuaded to adopt the virtual methods of promoting their product and service. I believe, however, that there is too much technological risk and misplaced confidence that a screen image, even if interactive, can replicate being there, to speak directly to someone and engage the five senses. Organizers that already are or intend to use virtual during the pandemic know that the revenue model for virtual is much less than live. A recent CEIR blog described the difference as “trading dimes for dollars”. Organizers know however that virtual will have to play a part in future tradeshows and conventions. How can they integrate it properly into traditional event formats and effectively monetize its features?

Many event organizers are planning a combination live and virtual program they call “hybrid’ for possibly the 3rd quarter of 2021 for some the hybrid format is viewed as a means of keeping their larger exhibition on everyone’s business agenda and schedule until the pandemic is brought under control and mass indoor gatherings resume. If successful the hybrid format may become the preferred event format. This will be a difficult cultural transformation for some event organizers. The switch from a high density setting with crowded aisles, plentiful face to face interactions be it buying, selling, questioning, networking, etc., to a controlled and technology-based environment will take a level of organization and finesse that is not in their playbook. In the long run the benefits should outweigh the risks in producing a hybrid event. Virtual could be a valuable and innovative supplement for many trade shows and association conventions alike. Denzil Rankine, Chairman of the consultancy, AMR International believes that:

Virtual will not recreate the intimacy of live and not all tradeshows will be viewings of art fairs and other cancelled events replicating their main elements virtually will spread. Virtual will not be just about maintaining contact with communities in the case of cancellations. When normal business resumes virtual will have earned its place, extending reach both during and also between events.

Alternative virtual event formats are either in development or already launched. As an example, one event organization I follow is the American Society of Hematology (ASH). ASH is a not-for-profit professional association. They and like associations differ from privately owned and operated tradeshows in that earning revenue from the event is secondary to their mission of advocacy, professional standards and training and as a conduit for professional contacts and research. ASH’s annual meeting was originally scheduled for early December at the San Diego Convention Center. It was cancelled and replaced with a complete virtual program on the same dates. Their program is rich and comprehensive with a full schedule including; general sessions, presentations of scientific papers, workshops, symposia, continuing education and exhibitor and product showcases. In preparation for this article I talked with Bill Reed, ASH’s Chief Event Strategy Officer. He related the importance of this event to their scientific and medical community. Normally attendance approaches 30,000. It is the seminal gathering for this profession. The success of this virtual format is essential for ASH as they have other events throughout the year. ASH’s use of virtual may extend further into the future than other events. Because their annual meeting is for health science professionals, they will be very cautious about live events until real progress is made to stop COVID – 19 spread. Other health science events will probably think likewise.

- Airline industry business problems such as fewer direct flights and inconvenient schedules as well as reluctance by professionals to fly will not be solved easily.

- Not to be overlooked, there is the common sense element of fear of infection easily brought about by a trip to a live tradeshow or convention. Safe within their routine of a secure office or plant where health regulations are rigorously enforced, employees going to a live event in a distant city face an infection risk at the airport, in the airplane, the taxi, the hotel, the city streets, the convention center, perhaps a restaurant and then the same places as the process reverses. Why would a company or an individual take that risk or even consider it until a vaccine has been invented and proved effective?

What Convention Centers Are Facing

An objective view for convention centers sees a grim future stretching into the 3rd or 4th quarter of 2021. Indeed, the unpredictable severity of the virus’s second wave and the uncertain timing of a vaccine are maddening conditions. For convention centers, many have been told to suspend business operations in order to help manage second wave effects. Meanwhile complementary industries and businesses are struggling to survive; airlines, hotels, event service companies, restaurants, and more. .

Some of a convention center’s financial risk has been offset by reductions in payroll with lay-offs, furloughs and salary reductions. Certainly utility and supply costs have been reduced also. For some there may be rental revenue from housing all the medical and other emergency services during the height of the pandemic. For now the same subsidy payments that have always supported convention center capital and operating budgets are in place. In the short run, when events resume, expect them to be smaller with less exhibitors and attendees and less earned revenue from rent and services. In the long term however, convention centers face a more serious problem. The pandemic has caused steep and troubling drops in hotel occupancy. The Hotel News Resource website reported US hotel occupancy hit a low point in March of 22%, then climbed to a high point of 50.1% in mid August. Presently it is about 49%. The occupancy rate for early September 2019 was at 71%. When you combine corresponding declines in RevPar and ADR, the result is a serious decline in hotel occupancy tax collection.

For convention centers these taxes support three essential financial functions:

- Debt Service Payments (if the fund source for center construction was revenue bonds) -The revenue source is normally hotel occupancy taxes sometimes supplemented by car rental or restaurant tax. Bond holders have to rely on income generated by the project to make interest payments. The income is a portion of the price of a hotel room. Investors regard this as more risky than general obligation bonds and the bonds generally pay a higher interest rate.

- Funding Capital Improvements – For convention centers this is often an expansion of space or building renovations

- Covering Operating Deficits – Most of the convention centers in the US rely on revenue transferred from hotel tax receipts or some other form of subsidy like a state tourism fund to cover operating losses.

Starting in April news reports about decreasing hotel occupancy began to surface. Now every week there are news reports of fewer hotel guests. These reports often include commentary about cities or states concerned about using reserve funds to pay debt service for convention center bonds. If the bond sale was well structured the reserve funds are designed to continue debt interest payments through difficult periods. I know of no circumstance where convention center bonds have defaulted nor forced to use reserve funds to pay scheduled interest payments. But we’ve never faced such a severe economic downturn before. However bond market analysts are beginning to sound the alert. Below is an excerpt from a report written by S&P Global Ratings titled “Outlooks On Certain U.S. Convention Center And Sports Authorities Revised To Negative From Stable On COVID-19 Impact”:

…..a prolonged environment of limited to no operations will greatly hamper the entities’ ability to meet debt obligations, as they do not have other significant stable revenue streams to rely on and generally have limited local authority to raise new revenues. Although we expect convention center authorities will do everything in their power to create environments that are conducive to hosting large gatherings and using their facilities, including contingency planning, altering operations and budgets projections, and working with local, state, and federal officials, their ability to do so may be largely out of their control if the current crisis persists.

Convention center managers should be most concerned about the lack of capital funds and coverage of operating losses. What will happen if the pandemic continues to limit hotel occupancy? What will happen if debt service takes all the hotel occupancy tax receipts? What can the convention center do to support itself? Convention center management has tried to increase earned revenue from rent and service fees and commissions, therefore decreasing the need for subsidies to cover operating losses. Some have been successful and achieved positive cash flow consistently. Few have been able to build a capital reserve for building improvements. This will become a major dilemma, possibly long term.

A convention center’s path to recovery will follow a similar path and trajectory as the event organizers. Know that it’s probable as bookings resume and events re-schedule, that space requirements, number of exhibitors and attendees will be reduced. Some events may be of fewer days. Expect most attendees to come from regions within reasonable driving distance, so overnight hotel stays will be less.

A Plan for Convention Center Management in the Interim

Board chairmen, CEOs and general managers should sense that now is a good time to devise a plan. Business is slowly returning, GDP and employment growth will consistently improve and the vaccine news is mostly favorable.

- First things first; achieve GBAC or equivalent certification for facility safety and cleanliness

- Assemble your team, key department and division heads, not too large. As a starting point, Finance will present a thorough data based report on current financial status vs. plan before the pandemic. Sales will do likewise.

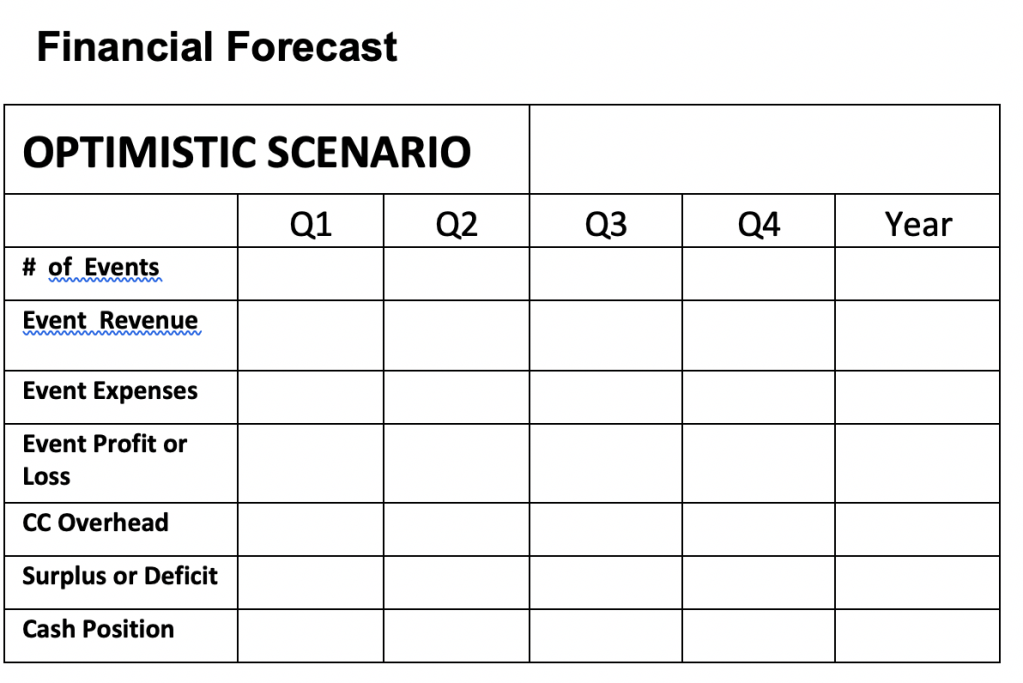

- Develop a list and fact based description of plausible scenarios. The scenarios should include an optimistic, pessimistic, a current momentum and a most likely case scenario. Each scenario should follow the same framework for issues and concerns outside the convention center’s control; the pandemic status, the vaccine development and deployment progress, government regulations and policy and the status of existing event clients. Example below:

Optimistic Scenario

COVID -19 – CDC forecasts a weak second wave for COVID – 19. However, they expressed concern about upcoming flu season and pressed states, regions and cities to aggressively promote flu vaccine shots within the next month

Vaccine – Trials are successful and deployment is ready to begin in the 1st quarter 2021

Gov’t – Restaurants will be cleared for indoor dining by 1st quarter 2021

Clients

- All of retained clients have made inquiries about resuming business in their normal date cycle by starting in late 2nd quarter 2021. Expect 15 -25% fewer exhibitors.

- Health Science events (there are 3) scheduled in 3rd and 4th quarter 2021 are still non – committal

- Lots of inquiries for consumer event clients, at least 20% more than 2018 and 2019.

4. Adapt the current business model (in place before the pandemic) to each scenario, Consideration should be given to the following:

- Expanding targeted markets to achieve greater occupancy. This “push everything through the front door” strategy is provocative and has risk, but such a compromise of sales strategy may be a necessity. You may be surprised what you find. A good example is how mid and small sized convention centers found certain indoor scholastic sports competitions a valuable market for earned revenue as well as out-of –town attendees.

- Review existing rent and service pricing. The market may well be highly competitive with competitors offering substantial discounts to regain market share.

- Review any capital funds remaining. Firstly, consider postponing any expansion plans you may have. You don’t need to build space you cannot fill. Think about improving the value of the space you have. Consider amending plans to accommodate expected event formats which have less exhibit space but more virtual and digital services. How can convention centers re-direct or obtain funding for improved communications infrastructure?

- Take on more services as building exclusives. This will cause controversy with event organizers who rely on commissions from service contractors they select. In the long run this is a fight worth fighting, especially with respect to high value services like electric. The convention center will need more revenue sources if subsidies become limited.

5. Plan on continually stress testing the business model adaptations against changing economic scenarios and frequent review of key performance indicators.

The Riddle of Pent Up Demand and the Sensibility of Face to Face Communication

Both pent up demand and face to face communications are inherent business concepts and part of our industry. There is no precise unit of measure to describe or quantify them, but there are available indicators that suggest their significance. I hope this narrative and explanation elicits an appreciation of their influence and importance.

Pent up demand is an inexact science but I know it exists in our industry..In my time at the Javits Center I experienced the power of pent up demand. The first time was when the business was reorganized in the mid 1990’s. At that time the center had an occupancy rate of about 39% trending downward. It was caused by a combination of corrupt, unproductive union labor and an absurd competitive event policy. The competitive event policy established long non-compete windows for existing events, in particular luxury goods, fashion and technology. Rapid reform of the labor issues and cancellation of the competitive event policy led to an occupancy rate of above 60% within two years and trending higher. Pent up demand came alive for us and did so dramatically. The second time was after 9/11. We had already begun to see strong weakening in net square footage use as a result of the dot- com bubble failure. In 2000 and 2001, the center

still had many technology sector clients as we witnessed their rapid decline. Then came 9/11. In the weeks following the attack we changed our marketing plan to include emphasis in other targeted event markets. The event inquiries and competition for dates were immediate. The result was 70% occupancy. I experienced pent up demand first hand but am ill-prepared to explain it properly. The thoughts and opinions of Scott Hoyt, a Senior Director at Moody’s Analytics, were helpful and are paraphrased below.

Pent-up demand is often discussed regarding consumer spending for durable goods such as appliances and automobiles. The US Bureau of Economic Analysis tracks these purchases nationwide and knows well the useful life of those products. When replacement spending does not meet forecast replacement as may happen during a recession, economists see this as a setting for pent up demand. The longer a consumer puts off buying a replacement, the stronger the desire to replace becomes. For other sectors such as business to business spending, there is no comparable unit of measure. However, a reasonable comparison can be made to the way consumer pent-up demand builds during a recession. Recessions are normally accompanied by higher household savings. Saving then falls during the recovery when consumers increase spending. This could easily compare with investors and large companies accumulating large cash reserves when there is high economic uncertainty as during a recession. The inference is that business spending behavior is similar to consumer spending behavior. In Scott Hoyt’s words, “consumers will lead the way.” Accepting that proposition, one can apply pent-up consumer demand for non-durable goods such as clothes and services such as vacations and discretionary medical procedures. Two services that come to mind are pricey vacations and going to the dentist. They are often put off during recessions, but come quickly back in focus as conditions improve.

There is another useful theory that uses the path spending would have taken with no recession. The approach assumes that income and employment had continued to grow and interest rates and unemployment were stable. So if CEIR forecasted 3.2% growth in the exhibition industry and a recession occurs, there would be a gap between forecasted and actual growth. Does the gap represent pent up demand? It is quite possible during a mild short lived recession, but our current economic downturn is so severe and long that profound changes in supply and demand would invalidate theory. It’s good to know what the target was though and use it as a benchmark. Pent up demand is an inexact science but I know it can be applied to our industry and its understanding will instruct and possibly guide us through recovery.

The Sensibility of Face to Face Communication

Face to face business dealings and transactions is a time honored concept dating back to the Middle Ages at mid-eastern bazaars or trade fairs in Europe. It has the quality of being able to see the other party close up and observe and read the way they express themselves not just through speech but also through facial expressions, body language and interactions with others. How else would one conduct business in an organized marketplace? The tradeshow, convention and consumer show is a business environment designed for personal contact and it has worked and grown successfully throughout the world.

Why is the emphasis on face to face communication so important? It’s not just the intimacy of speaking face to face. It’s also the direction a conversation can take, from the mundane to a shift for an esoteric idea that spontaneously grows into a business deal, an idea for a new product, an opportunity for business collaboration and more. It’s difficult to see this happening on Zoom. Some time ago Steve Jobs remarked that face to face communications would always be with us. He said, “There’s a temptation in our networked age to think that ideas can be developed by email and iChat. That’s crazy. Creativity comes from spontaneous meetings, from random discussions.”

There are other qualities and attributes of the role face to face communications plays at a tradeshow or convention:

- Communications is much clearer. It’s easy to misread and misinterpret information from a phone, email, text and even a video conference:

- Both verbal and non-verbal cues in a face to face meeting reveal something about the other party’s sincerity, trustworthiness and possibly more. These things are important and should cause you to research the facts and ideas from the conversation further.

- The conversation is more focused. The other party probably won’t be looking at personal messages on their cell phone as they probably do in a video conference.

- For a small business the opportunity to meet and talk leaders in the field and potential buyers of your product or service at a convention or tradeshow provides an accelerated path in marketing strategy

From The Plague by Albert Camus; “And indeed it could be said that once the faintest stirring of hope became possible, the dominion of plague was ended.”

Starting and Expanding Advertising and Sponsorships as a Revenue Stream

Why Is this a Good Idea?

I have often been confused why more convention centers do not actively engage in an advertising and sponsorship program as a revenue stream. Perhaps it’s viewed as a business more appropriate for others; sports and entertainment venues are the logical setting for advertising and sponsorships, not convention centers. Sports stadiums and arenas and their tenant teams – football, baseball, basketball, hockey, etc., all have a loyal fan base and fans are very emotionally connected. Television and radio coverage are integral parts of the sports experience. These things don’t exist at convention centers and convention center management may not feel it’s worth the effort. I also believe there’s reluctance by some convention center management to use ad space and media that were once exclusive domain of event managers and then, charge fees and commissions for features that were once free.

My belief is that if convention centers who feel this way would conduct a thoughtful evaluation of the benefits and risks, they may change their minds.

Benefits – A well crafted ad and sponsorship program:

- Contributes a level of legitimacy with respect to the convention center being a place of business, where new products and services are rolled out and demonstrated in a setting where comparisons can be made, where deals are done, where technical and scientific information exchanged, and where like minded professionals can network and socialize.

- Strengthens the business relationships with others in the city hospitality sector. Restaurants, hotels, nightclubs, shopping districts, and other cultural and entertainment venues are likely advertising and sponsorship candidates. Having the relationship solidified by an advertising agreement helps achieve that. The character of the relationship would be different; it won’t be casual or shallow anymore, it will now be business.

- Can become a reliable revenue source which may waver up and down with the vagaries of the economy but can grow in stable and growth years. There are a few convention centers where an advertising and sponsorship program has contributed between $1 – 2 million to the bottom line annually.

Risks –

- Know that many times brands are judged by the company they keep; remember this, it will come up again. Many times an advertiser or sponsor’s business issues, such as product problems, legal issues, and financial problems become your problems. This is especially true if it’s a naming rights sponsor. Choose potential advertisers and sponsors wisely. Understand that advertisers and especially sponsors may view the convention center similarly. Convention centers are accountable to them for bad publicity and for routine items such as signage and website maintenance, or for the overall condition of the facility. Sponsors too will always be interested in their return on investment and review the returns periodically.

- An overly aggressive ad and sponsorship program can pose some problems with your trade show and association meeting clients; too much signage by advertisers takes away from space available for an event’s trade dress signage and decoration and their own sponsor advertising, inflexible terms regarding advertising and product exclusivity by sponsors may interfere with an events’ exhibitors or their sponsorship sales. Also, critics may argue that over-commercialization with garish signage and endless brand messaging detracts from the convention center’s mission. It’s best to exercise good taste and a sense of propriety here.

- An advertising and sponsorship program is very visible to others and potential event clients. An ineffective and feeble program where advertisers and sponsors are few detracts from the center’s reputation. If, after evaluation, you do not believe you can achieve revenue goals and visibility then perhaps you should forego the effort.

Taking Stock – What Is Your Inventory of Advertising Possibilities and Media?

Exterior –

- The Center’s Location – Is it located by and in view of major traffic thoroughfares? If so, call the municipality and obtain a daily traffic count. Pedestrian counts may also be available.

- The Center’s Architecture – Normally the entrance is a piece of landmark architecture. The curtain walls are high, there is usually an array of light or flag poles along the entrance drive, and the adjacent sidewalks are wide. All are possibilities for banners and signage.

- Fixed Static or LED Signage (usually located by the center’s entrance) – These signs normally announce the event(s) in-house, but have fixed signage possibilities as part of the sign structure or in the case of an LED sign, use possibilities due to the technology.

Interior –

- Center entrance, atrium, lobbies and concourses – All have high curtain walls and space frame features for banner hanging

- Well trafficked corridors – Recommend a limited number of high quality back-lit signage

- Center video screens – Large video screens are best located in the expansive entranceways, atriums and lobbies where the scale fits the setting. Smaller video screens are more appropriately located along well trafficked corridors, retail areas, taxi/shuttle bus waiting areas and food courts. The screens are normally part of a network, complete with a control room, equipment room and the capability of running different messaging (pre-programmed) for each screen.

- Columns in atrium and lobbies

- Public stair risers – Normally temporary and done with 3M product with adhesive back

- Escalator side panels and railings

- Taut cables over escalator wells for banner hanging

- Displays adjacent to Information and Concierge Stations

- Ads and wraps at water coolers and phone/tablet charging stations

- Food Court table tops – Using the same adhesive backed 3M product

Digital/Print –

- The convention center’s website – Banner ads, column and button ads on the most popular pages (event schedule, public transportation and driving directions and map). A restaurant directory as well as one for hotels, nightclubs and other attractions should be part of the website. Some convention center websites do an excellent job of posting these directories. View the San Diego Convention Center’s restaurant directory:

http://www.visitsandiego.com/attendees/restaurants.cfm

- The center’s mobile app

- The center’s WiFi Portal (opening page)

- Blogs, newsletters, annual reports, direct mail pieces

- The center’s social media (Facebook page, Twitter Feeds, Instagram, YouTube, etc.)

- Exhibitor Manuals and Order Forms

Other –

- Opportunities to publicly display product – A luxury car in the center’s atrium is a good example

- Collateral reading material and brochures at concierge/information desks

- Portable cups and napkins in the food courts

Reserving Inventory Exclusively for Events – How much inventory should be reserved for them? The short answer is – any place public that has height and visibility (exterior, curtain walls, light poles, etc.). A well organized center will publish a guide with diagrams showing locations and standards for sign and banner hanging.

Charging Event Management Fees for Advertising Outside of Their Licensed Space – This is an excellent revenue source, at times comprising half of the center’s ad and sponsorship revenue. Most event managers already use most available locations. Besides their own trade dress and directional banners, in many instances they use these locations to sell advertising to their event sponsors, normally in the form of large fabric banners, stair risers, free standing displays, etc. Ten years ago most convention centers permitted events to sell ads to exhibitors using all the aforementioned media and signage without paying location fees to the convention center. I am pleased to see that many convention centers have ceased this practice and now charge fees and commissions. Convention centers which still offer this for free should be well advised to stop the practice. As controversial as it may seem, the architectural prominence and visibility that was created by public investment and the value it creates for such things as advertising banners gives convention centers clear entitlement to reasonable fees. Use of public areas for the sale of advertising to others is normally not part of the event manager’s license agreement. Fees should be a percentage of fees collected by the event managers from their client (say 15%). In the case of public space banners, the percentage arrangement is sometimes not satisfactory. For convention centers, it’s much easier to audit and collect based on size. Exterior banners should be charged a higher rate (say 20%). Ads for other media, such as the Center’s Wifi hotspot “splash” page, use of the Center’s monitors, food court table tops, etc. should be negotiated at market prices.

What’s the Difference between Sponsorships and Advertising?

A corporate sponsorship is a form of marketing where companies connect their name, brand, and products and services to a venue for long term in order to enhance their brand, solidify and expand their markets, showcase their products and achieve future profits. It should not be confused with advertising which is direct and overt and contractually a shorter term. In sponsorships, advertising through signage is inclusive, just one element in a sponsorship plan. A well designed sponsorship generates a stronger and more subtle message. It tends to be more qualitative and has loftier goals than just customer exposure and sales. It is a marketing platform where a company can identify with the best aspects of its partner, where a company can build credibility, prestige and, create a more permanent, lasting bond with consumers.

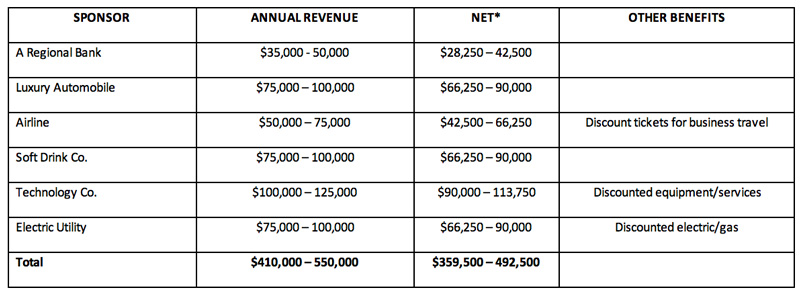

Who Are the Potential Sponsors?

It’s useful to first separate potential sponsors from ad hoc advertisers. Sponsors should be companies that have a tangible connection and can be easily integrated into a convention center’s core business and culture. There are however more subjective considerations. There has to be the proper feel and fit. It’s difficult to define but it comes down to whether the corporate image is one that complements the convention center, the city and vice versa. While the company should obviously be prosperous, they also need to have a certain brand reputation for reliability and quality, and a high corporate standard for civic responsibility.

Certain industries seem to fit as ideal sponsorship candidates. They are; an airline with a regional or national hub at the city’s airport, a major credit card company, a regional bank which has a solid customer and investment base in and around the city, a utility, a major technology/telecommunications company (preferably one that designs and manufactures, and operates equipment), a media company (preferably local newspaper or TV station), a luxury car company and a long standing major employer for the region. If your convention center is large and busy, then a soft drink sponsor, with exclusivity for advertising and product sales (pouring rights), also makes sense.

Some sponsorship marketing consultants, such as Jim Andrews from ESP Properties in Chicago (www.sponsorship.com) favor technology companies above others. His view is that these companies are in a growth mode, spend heavily on marketing and are generally open to venue sponsorships often seeking these opportunities out, particularly sports and entertainment venues. Another consultant, Hugh Wakeham from WAM Associates in Toronto (www.wam.ca/) believes similarly but also sees regional banks and utilities as excellent candidates. He described an interesting case study of naming rights where a utility company Enercare has naming rights to the convention center at Exhibition Place in Toronto. Enercare uses this sponsorship to demonstrate and promote Green technologies. On site for instance, windmills generate electricity and electricity, hot water/steam and chilled water are generated by a gas fired Tri-Generation power plant.

Sponsors will of course require something more than company name and brand exposure through signage. It is useful to have a list of other things that a sponsor could benefit from such as; exposure on your digital media (website, newsletters, blogs, twitter feeds and WiFi portal, etc.), free passes and parking to popular events that they can distribute to employees and clients, free use of public space to show or demonstrate a product, credits for rent, parking and F&B for an event like a corporate sales or board meeting. You may have to be creative here. As mentioned earlier sponsors pay close attention to their return on investment. There are items the convention center can track on their own such as product sales on site if applicable and hyperlink openings and page views. It is very likely that a sponsor may ask and possibly tie the result to renewal and fee negotiations. In my time at the Javits Center, it was common for our soft drink sponsor, Coke, to conduct a business review and focus on cases sold per year. The Director of Marketing and Communications at the Shaw Centre in Ottawa, Sylvie Carbonneau, described how their luxury car sponsor, Porsche/Audi, tracked sales based on their car displays at the centre.

For convention centers a successful sponsorship consists of cash and/or a capital contribution (which could be cash or in-kind – telecommunications/internet equipment for example), some accommodation for day to day operations (airline ticket credits for business travel or discounted utilities), cooperative marketing when these opportunities come up and a long contract term 3 to 5 years with renewal options.

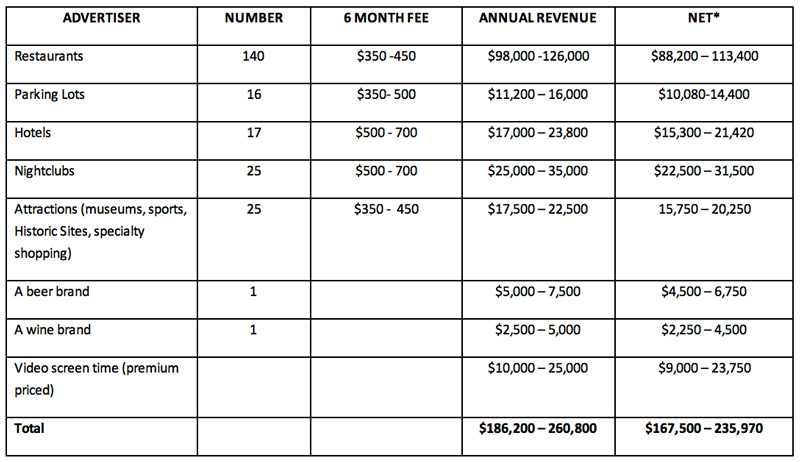

Who Are the Potential Advertisers?

A quick list should show the categories below and be accompanied by a map denoting walking time from the convention center and headquarter hotel (normally 15-20 minutes):

- Restaurants – These can be categorized by type of restaurant, ratings of same, price point and distance from major hotels and the convention center

- Hotels

- Parking Lots and Garages

- Shopping

- Nightclubs

- Attractions

- Professional Sports Venues

- Concert Venues

- Theaters

- Cultural Attractions (art galleries, museums, historical sites)

- Beer

- Wine

Other advertisers could be car rental companies, an office and hardware retail outlet, exhibit service companies – general decorating companies, exhibit appointed contractors, A/V companies, computer/technical supply retail outlets. Advertisers, especially in categories where there are many like restaurants, are typically put in easy to read directories which accessible through the center’s website, mobile app and WiFi portal. In my experience, advertisers normally didn’t track ROI closely. As with sponsorships, the convention center should track hyperlink openings and page views because it is likely that an advertiser may ask and possibly tie the result to renewal and fee negotiations.

A Sample Pro Forma

For the example below:

- Sponsor revenue is based on the Javits Center experience and informal conversations with other convention centers in my consulting business.

- Advertising revenue is based on my time at the Javits Center and price schedules from convention centers published on the internet. The number of restaurants, parking lots, hotels and attractions is based on those published on the Davis L. Lawrence Convention Center (Pittsburgh) website.

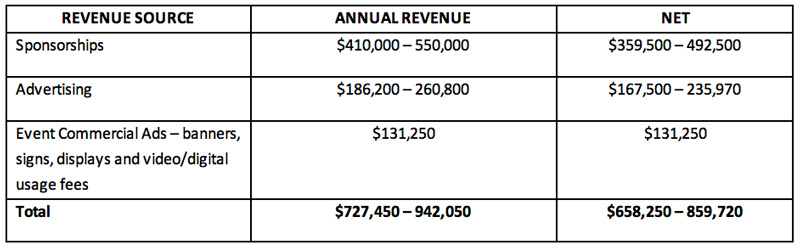

- Revenue obtained from fees for commercial advertising sold by event managers in public areas and video/digital media is estimated based on the Javits Center experience. Assume that the center’s occupancy in this example is high, say 60-65%. It was then estimated that 15 events would sell exhibitor advertising in public areas of the convention center;

10 events x $50,000 in sales = $500,000 5 events x $75,000 in sales = $375,000

$375,000 x 15% fee = $56,250 $375,000 x 15% fee = $56,250

$75,000 = $56,250 = $131,250 (estimated total)

*Venue obligation includes;

On-site signage, possibly on-site retail

On site video time – large and small screens

Product exclusivity, possibly advertising exclusivity (w/qualifications)

Website Ad

Social media exposure (Facebook, Twitter, Instagram, YouTube)

Mobile APP Ad

Rent, F&B, Parking Credits

Free passes to public events

Cost of above –

– Sales Comm – 5%

– Credits (lost revenue) – $5,000

*Venue obligation includes;

Website Directory

Social media exposure (Facebook, Twitter, Instagram, YouTube, etc.)

Advertising exclusivity for beer and wine

Mobile APP Directory

WiFi portal directory

Concierge/Information Booth Display and Menu Catalog

On site video time large and small screens – not included in 6 mo fee schedule above; pricing should be at premium levels

Cost of above –

– Sales Comm – 10%

How to Get Started – Logical Next Steps

Assuming you have already weighed the benefits and risks and reviewed the market size for sponsors and advertisers, these are logical next steps:

- Obtain price schedules from other convention centers that have an active advertising and sponsorship program in place.

- Build your own pricing model

- Build a pro forma statement

- Determine who will do all the administration and sales work. Understand that the sales work is hard work; developing marketing material, making cold calls, making site visits, and price negotiations. Add to that having patience; it will take more than a year to build revenue. Options are; outsourcing, Integrating the responsibility into existing sales force or add to staff with a new hire

- Obtain board approval in the form of a policy statement. This is important for two reasons; board members are a good resource for potential sponsors and advertisers and obtaining advertisers and sponsors may be regulated by government procurement procedures which really do not apply to this business function, board approval may help avoid this.

- From the city government, obtain traffic counts and pedestrian counts for adjacent streets and sidewalks. From your website administrator obtain internet traffic statistics. Invest in a survey to develop a demographic profile of attendees who normally come to events at the convention center. Typically they are business men and women between the age of 30 – 45 with a higher than average annual income.

- Develop marketing material. The link below from the Shaw Centre in Ottawa is a good example:

http://www.shaw-centre.com/wp-content/uploads/2015/12/SHAW-1527876_Advertising_Possibilities_EN.pdf

- Develop a face to face marketing message and a sales plan. The marketing message should be one of optimism, one that emphasizes positive changes such as an expansion or renovation, or an investment in video screens and digital technology, or the organizing of a staff to administer and look after the needs of sponsors. Persuade them of your resolve; show them that there is a parity of commitment, that the convention center has “skin in the game”.

- Begin work and monitor progress

All About Convention Center Naming Rights

Establishing Naming Rights Value

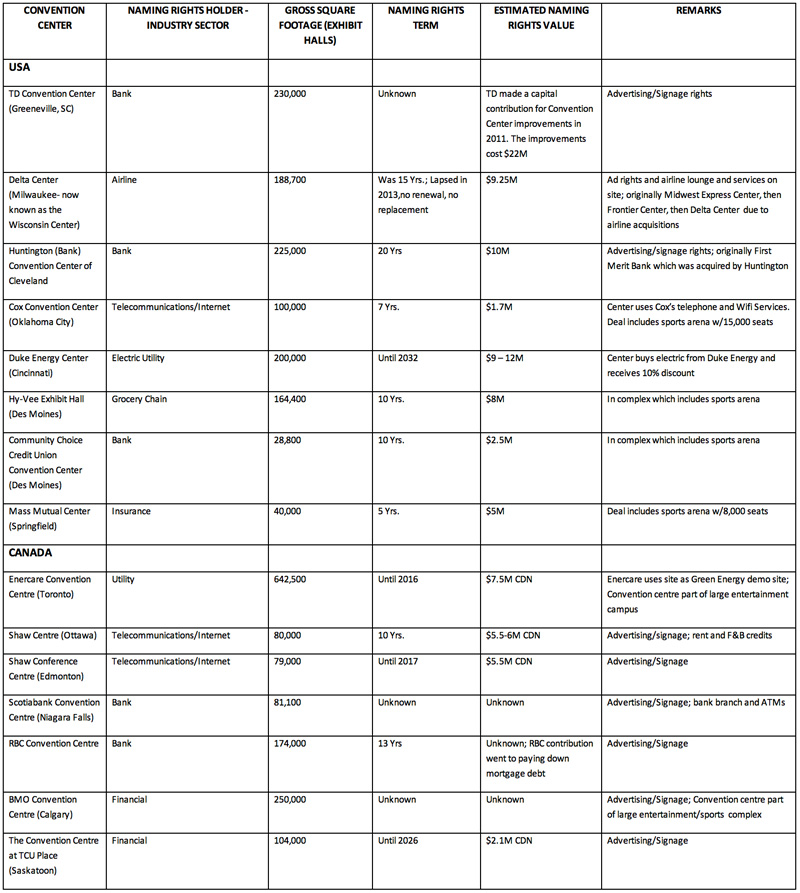

It’s easy to be lured into believing that naming rights as a financial bonus for convention centers. Decision makers may be influenced by media reporting and tend to overlook that only the global level deals are reported. They hear about deals like the Barclay Center ( Brooklyn Arena-Brooklyn Net home w/18,000 seats) valued at $200M over 20 years or the American Airlines Center (Home of NBA’s Dallas Mavericks) for $195M for 30 years. In these instances they must realize that the team’s market area is significant with a fan base which is loyal and reliable and stretches to anywhere television and radio can reach. Still, it’s hard not to think about the possibilities and I believe, beyond the blockbuster deals, at some point linear thinking takes over. They see their hometown arena achieve a significant naming rights deal in a small market area and they start thinking and believing their convention center can do likewise. As an example, the Chesapeake Energy Center in Oklahoma City (home the NBA’s Thunder w/18,000 seats) obtained a naming rights deal of $36M for 12 years. The Cox Convention Center across town has 100,000 sq. ft. of exhibit space and a 15,000 seat arena (w/ minor league hockey and an arena football team) and obtained a naming rights deal valued at $1.7M for 7 years, nothing linear about that. Linear thinking doesn’t work when comparing naming rights values to major league sports.

Linear thinking doesn’t appear to work when comparing the values of existing naming rights deals for convention centers either. If you study the table below you will see that it is very difficult to see any sense using valuation methods (cost, income or market valuation) when it comes to establishing a convention center’s naming rights value. The comparisons are too few, the market sizes and the venue sizes too diverse to see patterns. Additionally some relatively small markets have achieved surprising value; the HY-Vee Exhibition Hall in Des Moines is a good example ($8million with a term of 10 years).

From the current number of naming rights deals (14) the following characteristics are evident:

- Naming rights deals were closed during or after new, expanded or major renovations took place.